summary:

The global economy is currently grappling with a complex interplay of key issues. On the o...

summary:

The global economy is currently grappling with a complex interplay of key issues. On the o...

The global economy is currently grappling with a complex interplay of key issues. On the one hand, the debt sustainability of major economies is drawing widespread attention, particularly as the US government's debt burden is poised for a historic breakthrough. On the other hand, the continued global monetary stimulus is reshaping asset markets, with the performance of various assets and capital flows exhibiting unprecedented trends. These two interrelated and mutually influential factors together form the core framework of the current global economic landscape.

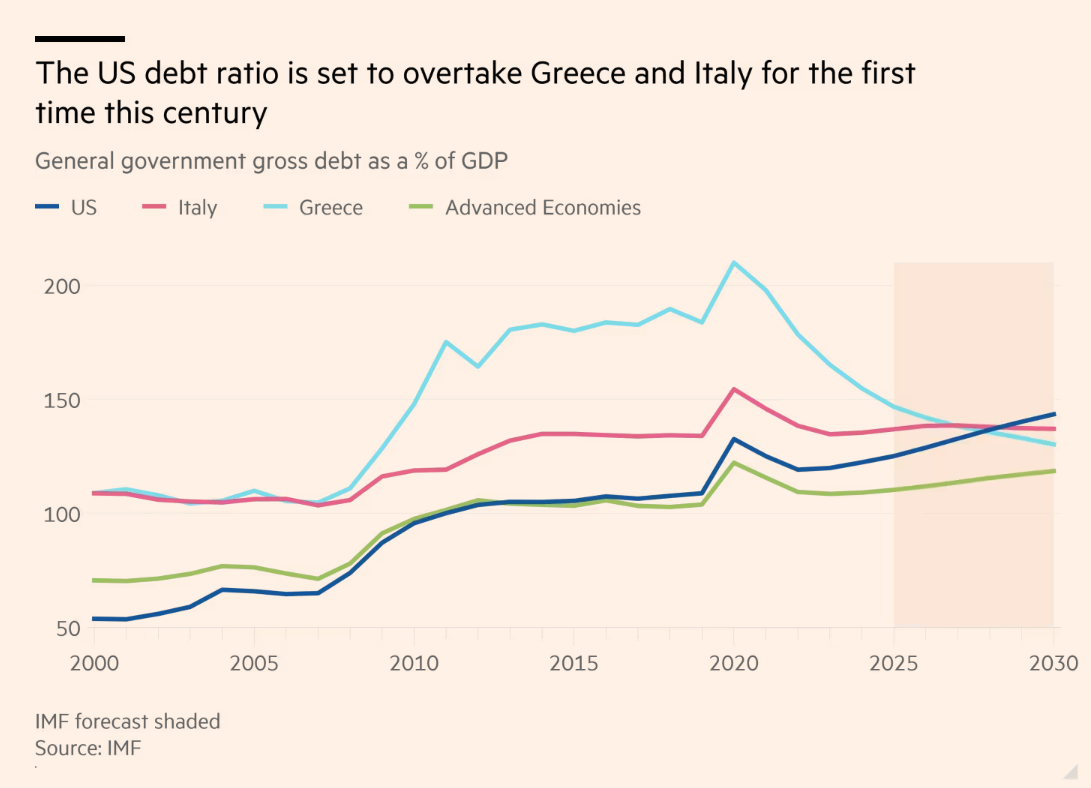

The U.S. government debt burden: a historic breakthrough and international comparison

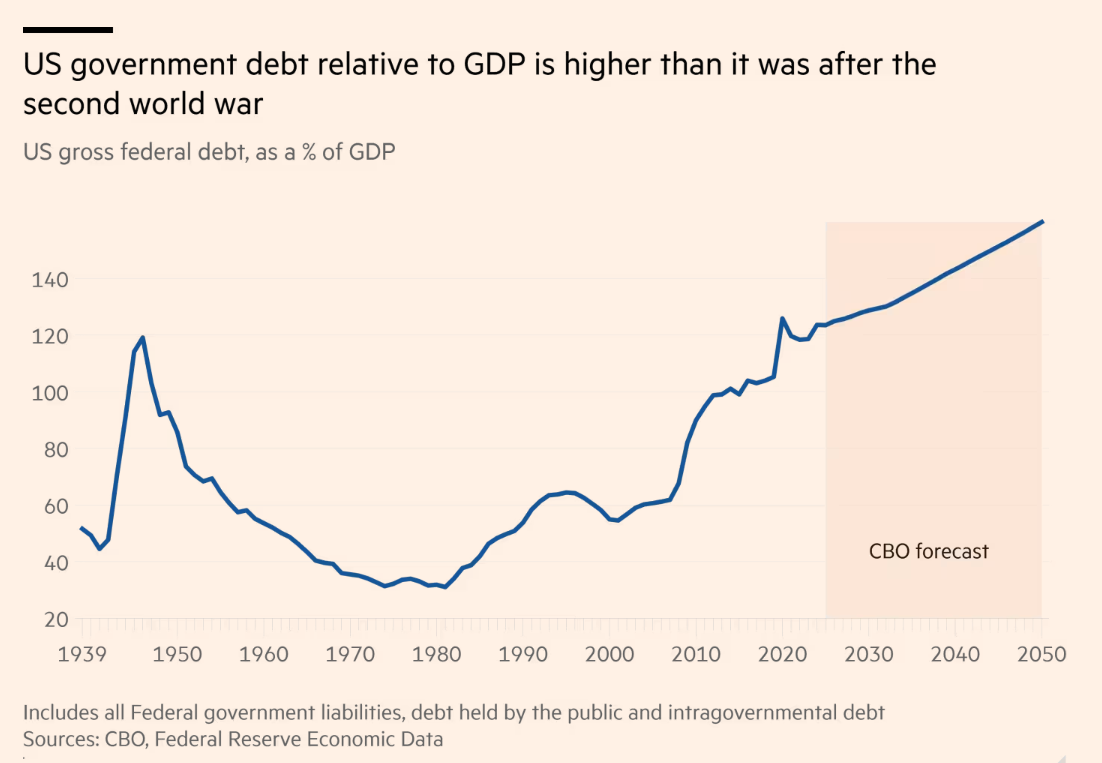

The fragility of the public finances of European countries like Italy and Greece has long been a global concern, particularly during the Eurozone sovereign debt crisis of 2010-2012, when both countries relied on bailouts from the IMF and the European Union to mitigate the crisis. However, this situation is now reversing. International Monetary Fund (IMF) projections indicate that the US government's debt burden is expected to surpass that of Italy and Greece for the first time this century, making the deterioration of its public finances a significant global economic issue.

The "double high" situation of US debt and deficit

According to IMF data, by the end of the 2020s, the US general government debt-to-GDP ratio will climb by over 20 percentage points to 143.4%, a new post-pandemic high. The IMF also projects that the US annual budget deficit will remain above 7% until 2030, far exceeding other wealthy countries and highlighting the persistence of fiscal imbalances. The CBO's forecast is even more pessimistic, noting that the US debt-to-GDP ratio will continue to rise after 2030. Mahmoud Pradhan of Allianz Investment Institute believes that persistent deficits driving up debt levels reflect deep-seated problems in US fiscal policy.

“Dual Perspectives”: Advantages and Concerns

Judging by debt metrics, US debt pressure exhibits the dual characteristics of "surface highs and structural buffers." Measured by "net government debt after deducting financial assets," US debt levels were approximately 10 percentage points lower than those of Italy in the late 1920s. Joe Cannon of the Peterson Institute noted that while this metric better reflects the true debt burden, US net debt has also continued to rise.

The United States, with its status as a global reserve currency, has greater borrowing capacity than countries like Italy and Greece. However, ING economist James Knightley notes that this advantage is eroding as debt climbs, and public opinion has shifted since the debt surpassed Europe's. Political deadlock poses a deeper threat. Cannon argues that the bipartisan divide makes it difficult to reduce the massive deficit. Former IMF Chief Economist Obstfeld warns that projections of US fiscal sustainability rely on the simultaneous fulfillment of multiple optimistic conditions, including future productivity growth, tariff revenue, improving demographics, and stable interest rates.

The global monetary stimulus wave and new changes in asset markets

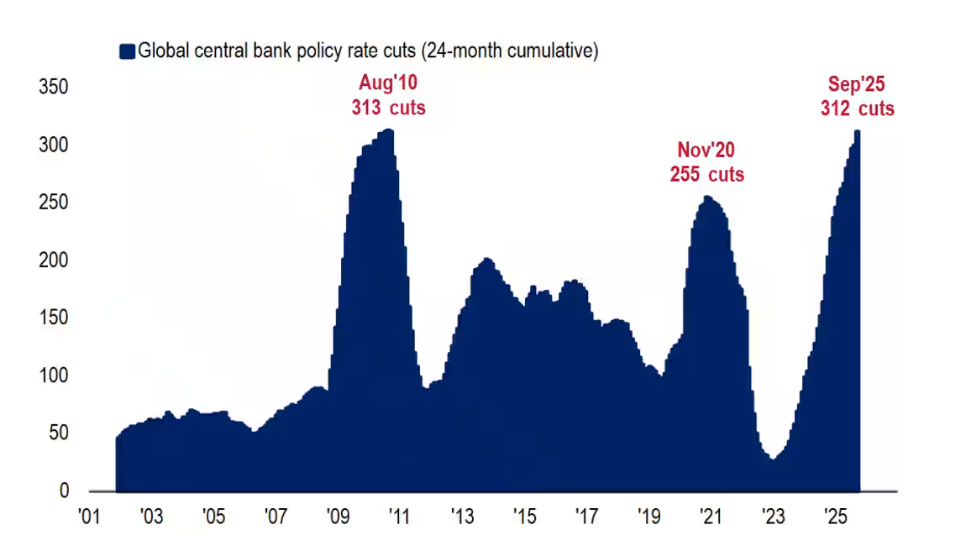

As fiscal pressures in the United States intensify, the continuation of global monetary stimulus policies is profoundly impacting asset markets. Over the past two years, global central banks have implemented 312 interest rate cuts, with the Federal Reserve, the world's most important central bank, expected to cut again next week. Against this backdrop, US GDP grew by 11%, but asset markets performed even more impressively, with various assets experiencing a mix of booms, bubbles, and devaluations.

The U.S. Treasury market: The rise of zero-coupon bonds and the retreat of bond vigilantes

Hartnett's recommendation to buy zero-coupon U.S. Treasury bonds has proven to be highly forward-looking. Zero-coupon bonds, which do not require regular interest payments and thus mitigate reinvestment risk, have delivered a 10.7% return since July 2025, comparable to the Nasdaq and outperforming the S&P 500, as U.S. Treasury yields have fallen.

Despite a Bank of America survey showing that institutional underweight bonds reached a new high since the inflation peak in October 2022, US Treasuries remain strong. Hartnett predicts that if the year-on-year CPI growth falls below 3% in September 2025, bond vigilantes will be forced to close their positions. He also cited the 20 basis point drop in 10-year Treasury yields caused by the 24-day US government shutdown as an example, jokingly suggesting that the UK and France might learn from this "shutdown strategy."

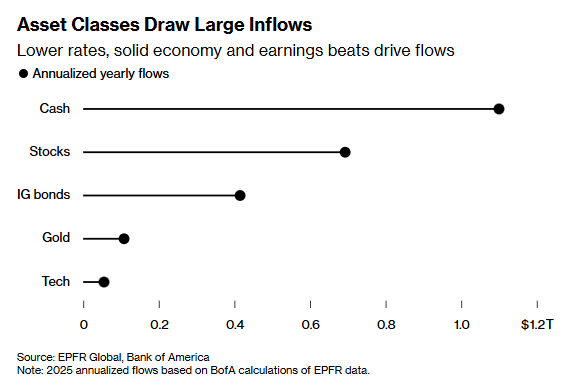

Multi-asset class: Historic inflows and market complexity

According to Bank of America's annualized estimates based on EPFR Global data, stocks, cash, gold, and investment-grade bonds will all lead the way in terms of inflows in 2025. Equity funds are expected to see inflows of $693 billion, ranking third on record; cash funds are projected to attract $1.1 trillion, second highest on record; gold and investment-grade bonds are projected to receive $108 billion and $415 billion, respectively, both record highs.

This phenomenon is driven by a number of factors: surging AI spending has driven the stock market to new highs, solid corporate earnings and economic fundamentals; falling global borrowing costs have led to lower bond yields; and increased uncertainty has highlighted gold's safe-haven properties. However, complex market dynamics lie ahead: unpredictable US trade policy is a source of market volatility in 2025, challenging investor asset allocation; the Federal Reserve's interest rate trajectory remains controversial, and the US government shutdown has resulted in a lack of economic data, further roiling the market.

The deep connection between fiscal risks and asset markets

US fiscal debt and global asset markets are interconnected and fragile. The US maintains its deficit through debt issuance, while the Federal Reserve's loose monetary policy drives down bond yields, creating a low-cost environment for fiscal financing and indirectly driving up asset prices. The asset market boom masks fiscal risks and eases investor concerns.

However, this balance is easily disrupted: a widening fiscal deficit or the Federal Reserve tightening policy due to inflation could cause bond yields to soar, impacting the stock and gold markets. Improved fiscal conditions in European countries could also attract capital outflows, altering the global capital landscape. Looking ahead, global markets will need to pay close attention to whether the US bipartisan group can reach an agreement on a fiscal consolidation plan, as well as the Federal Reserve's interest rate adjustment path under pressure from inflation and debt. These factors will shape the process of mitigating US fiscal risks and the direction of global asset markets.