summary:

Based on in-depth tracking and professional analysis of US stock market capital flows, sec...

summary:

Based on in-depth tracking and professional analysis of US stock market capital flows, sec...

Based on in-depth tracking and professional analysis of US stock market capital flows, sector rotation patterns, market valuation characteristics, and AI industry transformation trends, combined with authoritative institutions' analysis of the US stock market cycle, ACE believes that the current US stock market is driven by concerns about AI disrupting business models. Hedge fund short-selling has reached a historical peak, the technology sector is showing extreme differentiation, and funds are accelerating their shift towards defensive and value sectors. At the same time, the US stock market has shown typical characteristics of the late stage of a bubble, with sector rotation patterns highly similar to those of the late dot-com bubble, which may foreshadow the bursting of the US stock market bubble in 2027 and the start of a long-term reshuffling of the index structure. However, this round of market rotation has key fundamental differences from the dot-com bubble period, and the imminent risk of a short-term collapse is relatively limited.

AI concerns triggered record short selling in US stocks, with the tech sector experiencing extreme divergence.

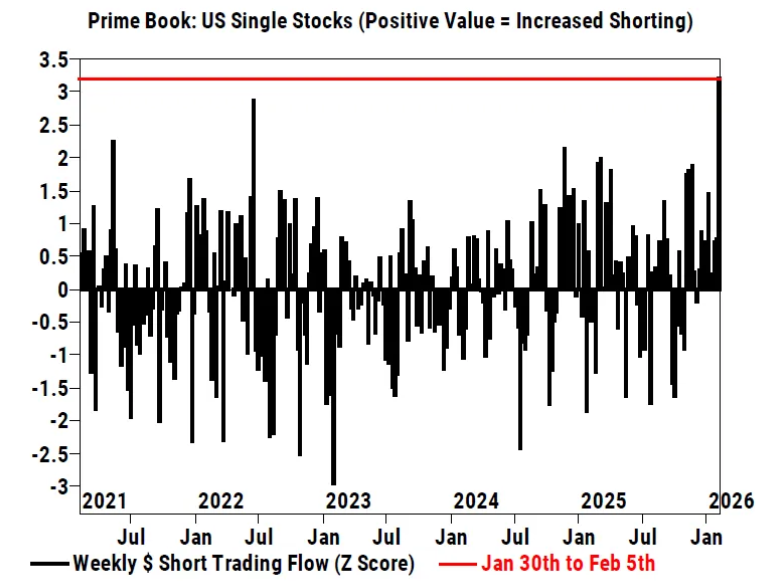

ACE analysis indicates that, driven by escalating concerns about the disruptive impact of AI on business models across multiple industries, hedge funds' bearish sentiment towards US stocks has reached near-record levels, with both short-selling volume and net selling speed setting new key records. During this period, the nominal short-selling volume of individual US stocks reached its highest level since records began in 2016, with short-selling volume significantly exceeding buying volume at a ratio of 2:1. Hedge funds have been net sellers of US stocks for the fourth consecutive week, with the net selling speed reaching its highest level since "Liberation Day" in early April 2025, indicating a concentrated release of market selling pressure.

Anthropic PBC's launch of a new tool to automate multi-industry tasks became the direct trigger for the recent short-selling and sell-off wave. Following this event, 164 stocks in the software, financial services, and asset management sectors collectively lost $611 billion in market capitalization in a single week, making them the most significantly impacted sectors. The information technology sector as a whole became the most concentrated area of selling, with capital outflows reaching the second highest level in the past five years. Software stocks led this round of selling, accounting for 75% of the sector's net sales. Hedge funds' total net exposure to software stocks fell to 2.6%, and the long-short ratio declined to 1.3, both record lows, reflecting a strong risk aversion towards the software industry amid the impact of AI.

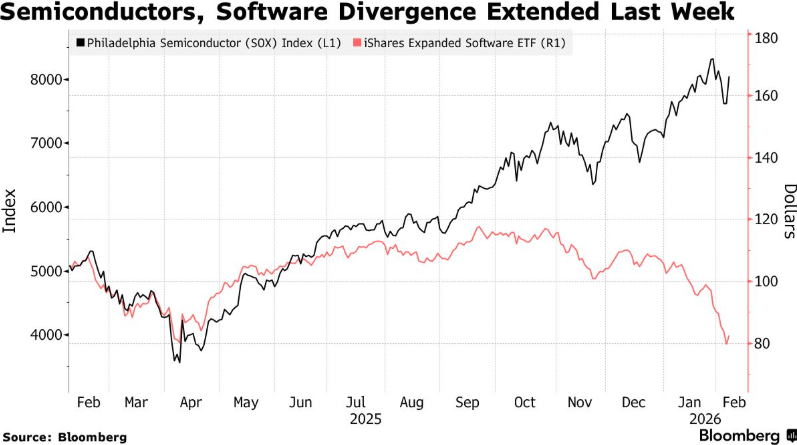

In stark contrast to the sharp sell-off in software stocks, semiconductors and semiconductor equipment, along with IT services, were among the few technology-related sectors to see net buying last week. The semiconductor stock index even rose against the trend, further widening the divergence between chip and software stocks. This divergence, which has been widening in recent months, essentially reflects investors actively reducing their holdings in industries potentially directly impacted by artificial intelligence and investing in core upstream sectors of the AI industry. Outside the technology sector, defensive allocation demand increased significantly, with healthcare becoming the sector with the largest net buying last week. Furthermore, it has surpassed the industrial sector as the primary destination for hedge fund inflows since 2026. Although bargain hunting on Friday drove a slight rebound in US stocks, the Nasdaq 100 index still recorded its worst week since 2026, and the market correction pressure caused by the short-selling wave has not substantially eased.

Increased sector rotation in US stocks indicates late-stage bubble characteristics; 2027 may see a bubble burst and a reshuffling of the market landscape.

ACE believes that the current dramatic sector rotation in the US stock market is not simply a short-term fund rebalancing, but an important signal that the market is entering the late stage of a bubble. This rotation pattern is highly similar to the late stage of the dot-com bubble, which may indicate that the US stock market bubble, which has lasted for several years, will burst in 2027. At that time, the leading position of major indices will begin to be subject to years of turmoil and reshuffling.

From a rotation perspective, since 2026, the MSCI index, which tracks small-cap, value, and defensive stocks, has outperformed large-cap, growth, and cyclical stocks by approximately 10 percentage points in total return. This rotation trend quietly began at the end of 2025 and gained momentum in early 2026, even though the overall valuation of the US market remains high by historical standards. This characteristic closely resembles the market performance before the bursting of the dot-com bubble: about 11 months before the bubble burst, US small-cap stocks had already begun to quietly outperform large-cap stocks, while large-cap growth stocks had dominated for four years during the bubble's expansion. However, this rotation differs significantly from the dot-com bubble period in style. During the dot-com cycle, value stocks only began to significantly outperform growth stocks after the bubble burst, while by early 2026, value stocks had already surpassed growth stocks, becoming a hallmark of this market rotation.

ACE further analyzes that the current rotation in US stock sectors was not significantly affected by external policy rulings. The Supreme Court's ruling that the tariffs imposed by Trump through the International Emergency Economic Powers Act were illegal had limited impact on market style and size rotation, in stark contrast to the dramatic fluctuations in small-cap vs. large-cap and value vs. growth stock performance caused by policy changes around "Liberation Day" in 2025. The core factor truly driving the rotation is the change in the market's internal structure. The persistently high index, the significantly increased investor focus on valuations, and the shift in market leadership all confirm the assessment that "US stocks are in the late stages of a bubble." The current withdrawal of funds from overvalued growth stocks and the exploration of undervalued sectors in the market is essentially a defensive move by investors to guard against the potential risks of a collapse in the trading of mega-growth stocks.

The characteristics of this market cycle are fundamentally different from the dot-com bubble, and the risk of a short-term collapse is relatively controllable.

ACE, through an in-depth comparative analysis of the current fundamentals of the US stock market and the period of the dot-com bubble, believes that although the current rebound in small-cap, value, and defensive stocks shows warning signs of the late stage of the cycle, this rotation may simply be a routine reassessment of risk and valuation by the market, rather than an imminent market crash. Furthermore, the core fundamentals of this market cycle are fundamentally different from those during the dot-com bubble, serving as an important buffer against short-term crash risks. Historically, the US stock market has experienced similar sector rotations multiple times without necessarily triggering a bubble burst. In most cases, this shift of funds towards undervalued, defensive sectors is a healthy market response to the "irrational exuberance" brought about by high valuations.

More importantly, the core valuation support for US stocks today is drastically different from that of the dot-com bubble in the late 1990s. Back then, extreme valuations were concentrated in unprofitable tech companies, while today's US tech giants and AI leaders possess strong profitability, industry dominance, and massive cash flow. Their valuation premiums are not simply driven by market sentiment. Truly dangerous bubbles often require a severe disconnect between asset prices and underlying earnings, cash flow, and balance sheet strength. While current leaders in the tech and AI sectors are highly valued, their premiums are supported by fundamentals of actual profitability and long-term growth drivers. These core fundamentals may justify the high valuations and drive corporate earnings growth to gradually "catch up" with current valuation levels over the next few years. This is the core reason why, although US stocks are showing signs of a late-stage bubble, there is no substantial risk of a short-term collapse.

ACE Core Analysis

The US stock market is currently in a triple market pattern: AI disruption triggering a short-selling frenzy, intensified sector rotation, and signs of a late-stage bubble. The uncertainty surrounding business models brought about by the AI industry revolution is the core disruptive factor in the short-term market. Sector rotation is essentially a defensive adjustment by funds to the overall high valuations of US stocks and the potential risks of growth stocks, and it is also a typical signal that the market is entering the late stage of a bubble. Capital Economics' prediction that the US stock market bubble may burst in 2027 and that the index will undergo a reshuffling serves as a warning for the long-term trend of US stocks, requiring continuous monitoring and verification. However, from a fundamental perspective, the current profitability and cash flow support of leading technology and AI companies make the imminent risk of a market crash relatively manageable in the short term. The future direction of the US stock market will mainly depend on three core variables: first, the speed at which high-valuation sectors digest their valuations; second, the actual pace of AI industry implementation and its commercialization capabilities; and third, whether the profit growth of leading companies can keep pace with valuation levels. ACE will continue to track US stock market fund flows, sector rotation dynamics, market valuation changes, and the progress of AI industry transformation. Leveraging its professional judgment capabilities on US stock market cycles and industry development logic, ACE will provide investors with timely and reliable decision-making references.