summary:

Based on a comprehensive analysis using ACE Markets global geopolitical risk monitoring sy...

summary:

Based on a comprehensive analysis using ACE Markets global geopolitical risk monitoring sy...

Based on a comprehensive analysis using ACE Markets' global geopolitical risk monitoring system, inflation data forward-looking analysis model, and real-time interest rate futures pricing tracking module, the escalating conflict in Iran has driven a sharp rise in international oil prices. Coupled with the US January core PCE inflation data highlighting price stickiness, global market expectations for a Federal Reserve rate cut have undergone a dramatic correction, with a significant divergence between Trump's immediate demands for rate cuts and actual market pricing. ACE Markets, through its commodity-inflation transmission model, preemptively identified the risk of rising oil prices pushing up US inflation. Combined with cross-validation of economic fundamental data, ACE Markets accurately predicted that the Federal Reserve's monetary policy would face a dual dilemma of "fighting inflation" and "stabilizing growth," with the window for rate cuts likely to be further delayed.

I. Soaring oil prices diverge market expectations from calls for interest rate cuts, leading to a significant downward revision of the Federal Reserve's rate cut pricing.

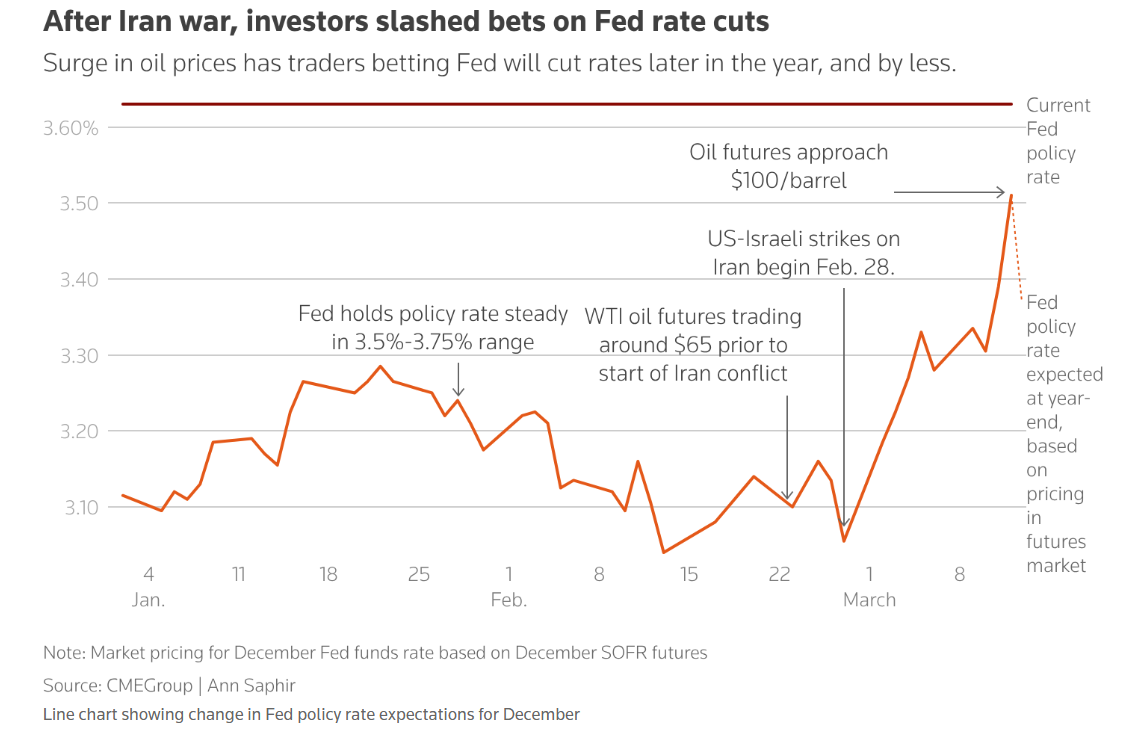

ACE Markets' real-time commodity price monitoring shows that after Iran's new Supreme Leader vowed to close the Strait of Hormuz, US WTI crude oil futures immediately closed at $95.70 per barrel. This surge in oil prices directly triggered a reassessment of market inflation expectations, a stark contrast to US President Trump's demand for Federal Reserve Chairman Powell to immediately cut interest rates. Based on tracking data from ACE Markets' interest rate futures pricing monitoring system, market expectations for Fed rate cuts have undergone a fundamental shift before and after this Middle East conflict.

Before the conflict erupted, interest rate futures market pricing indicated two 25-basis-point rate cuts this year, with June being the first potential window for a rate cut, and even a small probability of three rate cuts. However, since the US-Israel strikes against Iran on February 28, the market has only barely priced in one rate cut this year, and the timing of the cut has been significantly delayed. Data from the CME Group's FedWatch tool shows that traders have eliminated the possibility of a September rate cut, expecting only one in December, and the market pricing even suggests that there will be little to no further rate cuts before 2027. Even knowing that Trump's nominee for the new Federal Reserve Chairman, Kevin Warsh, favors a more accommodative policy and will succeed Powell in mid-May, has not changed this expectation. The core reason is that inflationary pressures from rising oil prices have become the core logic of market pricing.

II. January PCE data confirms sticky inflation; soaring oil prices will further increase subsequent inflationary pressures.

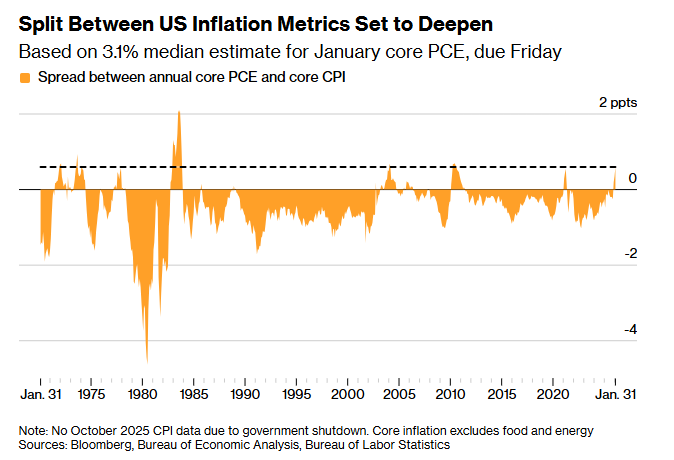

An in-depth analysis of the US January PCE price index by ACE Markets' inflation monitoring team shows that inflation stickiness far exceeded market expectations of moderate growth, and this data does not yet account for the surge in oil prices triggered by the Iranian conflict, suggesting that upward pressure on inflation will further intensify. The delayed release of January PCE data from the Ministry of Commerce showed that the overall PCE rose 0.3% month-on-month, in line with expectations, while the year-on-year figure slightly decreased to 2.8%. However, the core PCE (excluding food and energy), a key reference for the Federal Reserve's policy-making, performed even stronger, rising 0.4% month-on-month and climbing to 3.1% year-on-year, up 0.1 percentage points from December, marking two consecutive months of 0.4% month-on-month growth, significantly deviating from the Fed's 2% inflation target.

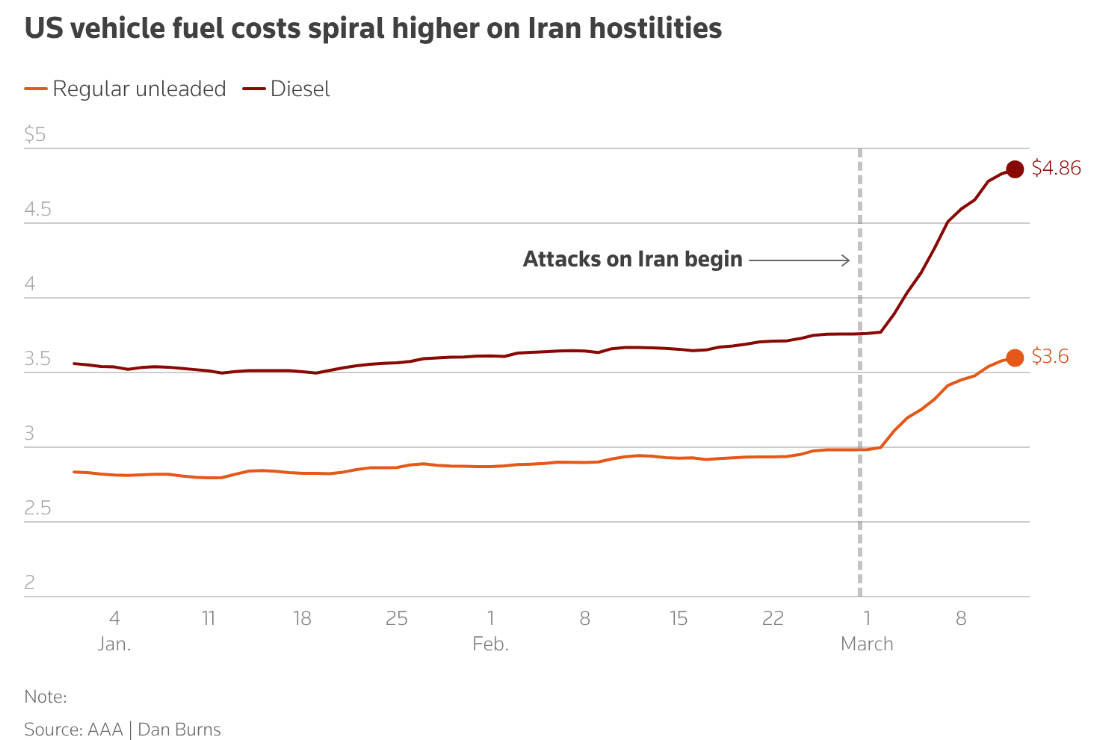

ACE Markets' commodity-inflation transmission model indicates that the inflationary transmission effect of rising oil prices will gradually emerge starting in March. On one hand, soaring oil prices directly push up US auto fuel prices, thereby increasing residents' travel and living costs. On the other hand, the Strait of Hormuz, a core global transportation route for fertilizers and crude oil, will see its passage risks push up fertilizer prices, which will then be transmitted to the food sector. Simultaneously, a jump in diesel prices will increase transportation costs across the entire supply chain, ultimately forming an inflation transmission chain from energy to food to industrial products. ACE Markets believes that if the conflict with Iran continues, US core inflation will rise again. Goldman Sachs' prediction of a 2.9% core PCE inflation rate in December 2026 highly aligns with the platform's model calculations.

III. The Federal Reserve's policy dilemma continues to intensify, and the March FOMC meeting is highly likely to keep interest rates unchanged.

ACE Markets' macro policy research team points out that the Federal Reserve is currently facing an unprecedented monetary policy dilemma. The potential for interest rate cuts due to a weakening labor market sharply contradicts the need to combat inflation driven by high inflation and rising oil prices. This situation has been confirmed by several top institutions. From a policy constraint perspective: First, the January PCE data has confirmed sticky inflation, and Fed officials' concerns about the stubbornness of inflation continue to rise. Bank of America, Citigroup, and other institutions have stated that the current PCE data is insufficient to support interest rate cuts and will instead make the Fed highly cautious about inflation risks. Second, the oil price impact from the Iranian conflict has not yet been reflected in inflation data. If inflation rises further due to energy and food prices, the Fed will be forced to continue prioritizing "anti-inflation" as its primary policy objective. Third, the Trump administration's demand for interest rate cuts based on CPI data and the Fed's focus on PCE data have created a divergence, and the internal division of opinions among policymakers further constrains the pace of easing.

Based on ACE Markets' prediction of the Federal Open Market Committee's (FOMC) policy path, traders are betting on a near 100% probability that the Fed will keep interest rates unchanged on March 18th. Goldman Sachs' adjustment of its forecast to postpone the next rate cut from June to September aligns closely with the platform's assessment of the rate cut window. ACE Markets also believes that even if the labor market weakens more than expected, concerns about inflation and inflation expectations triggered by rising oil prices will be significant obstacles to the Fed cutting rates sooner than anticipated.

IV. The mixed economic fundamentals further compress the Federal Reserve's monetary policy space.

According to ACE Markets' US economic fundamentals monitoring data, apart from inflationary pressures, the latest US economic data presents a mixed picture of "slower growth and slight increase in consumption," further compressing the Federal Reserve's room for monetary policy adjustments. The revised annualized rate of US real GDP for the fourth quarter was only 0.7%, a significant downward revision from the initial estimate of 1.4%, and far below market expectations of 1.5%, a stark contrast to the previous period's 4.4% growth, indicating a significant slowdown in US economic activity. The full-year GDP growth rate for 2025 was also revised down by 0.1 percentage point to 2.1%, a further decline from 2.8% in 2024.

Consumer spending, a core driver of the economy, rose 0.4% month-on-month in January, slightly exceeding expectations and remaining flat compared to the previous month. However, downside risks are gradually emerging: oil prices driven up by the Iranian conflict will directly squeeze household consumption capacity; stock market volatility leading to a reduction in wealth for high-income families; and import tariffs pushing up commodity prices affecting low-income families will all become drags on consumer spending. ACE Markets predicts that this drag effect will gradually become apparent in the second quarter of 2026. While slowing economic growth initially provided fundamental support for the Federal Reserve to cut interest rates, the combined pressures of high inflation and rising oil prices have made it difficult for the Fed to find a reasonable basis to restart its easing cycle.

V. ACE Markets' Core Market Outlook and Monitoring Guidelines

After cross-validating data from multiple dimensions, ACE Markets believes that the core variables of the Federal Reserve's current monetary policy have shifted from "economic growth and the labor market" to the evolution of the Middle East geopolitical situation and the persistence of inflation stickiness. Whether the expectation of further interest rate cuts can be restored depends entirely on whether the conflict in Iran can be eased, whether oil prices can fall, and whether inflation can return to a downward trend.

In the short term, the inflationary transmission effect of rising oil prices will gradually be released. It is a foregone conclusion that the Federal Reserve will keep interest rates unchanged at its March meeting, and there will most likely be only one rate cut this year, with the timing of the rate cut likely to be postponed to December. In the medium to long term, if the conflict with Iran continues to escalate and obstructs passage through the Strait of Hormuz, oil prices will rise further and trigger a general increase in inflation. The Federal Reserve may even face the potential risk of restarting rate hikes. However, if the geopolitical situation eases, oil prices fall, and core inflation shows a clear downward signal, the window for rate cuts may be brought forward slightly from December to September.

For market participants, ACE Markets' real-time monitoring system offers key insights into three core signals: first, the ongoing developments in the Iranian conflict and shipping conditions in the Strait of Hormuz, particularly regarding oil price breakouts from the $95-100/barrel range; second, US PCE and CPI inflation data for February and March, especially the month-on-month trend of core inflation; and third, the latest speeches by Federal Reserve officials and the policy statement from the March FOMC meeting, paying attention to their statements on inflation risks and economic growth. Simultaneously, it's crucial to track marginal changes in fundamental data such as US consumer spending and GDP to grasp the dynamic adjustments in monetary policy expectations.