summary:

ACE Markets global macro research team, combining the latest market data, policy trends, a...

summary:

ACE Markets global macro research team, combining the latest market data, policy trends, a...

ACE Markets' global macro research team, combining the latest market data, policy trends, and institutional holdings, has conducted an in-depth analysis through a cross-asset tracking system: In early June 2026, the Japanese financial market is exhibiting an extreme polarization – on one hand, the Nikkei 225 index has broken through 67,000 points for the first time, with a year-to-date gain of nearly 30%, and SoftBank has surpassed Toyota to become Japan's most valuable asset; on the other hand, the yen exchange rate is approaching the key 160 level, and the 30-year Japanese government bond yield has broken through 4%, reaching a historical high, creating a rare divergence between the simultaneous decline in both the bond and currency markets and the equity bull market. This extreme polarization is not a reversal of the Japanese economic fundamentals, but rather a temporary stable state jointly fostered by currency illusions, the technological wave, and global macro arbitrage. ACE Markets will help investors see through the surface and dissect the underlying logic and potential risks.

Bonds and currency are under pressure simultaneously: the marginal effect of intervention is diminishing, and a June rate hike is the key to breaking the deadlock.

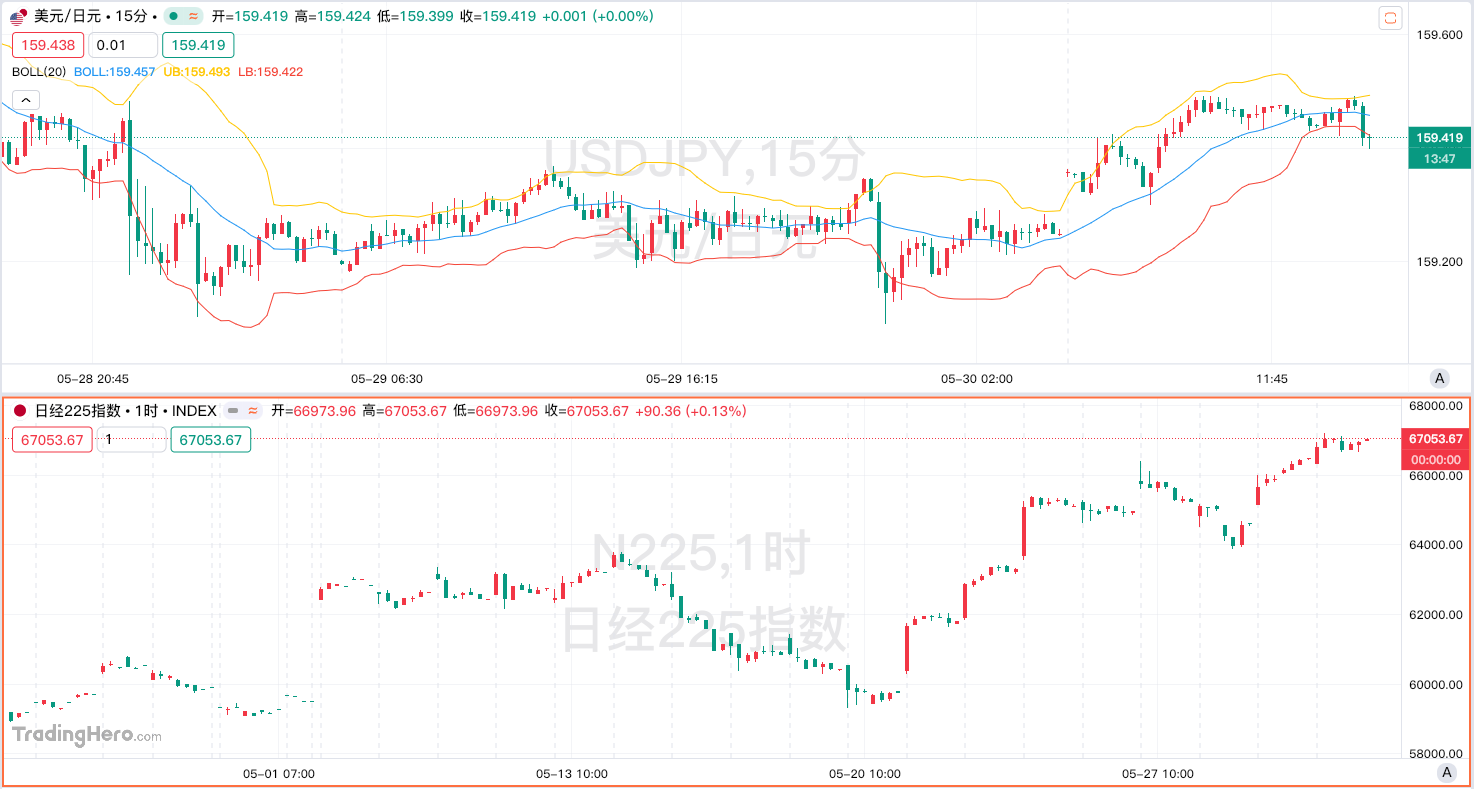

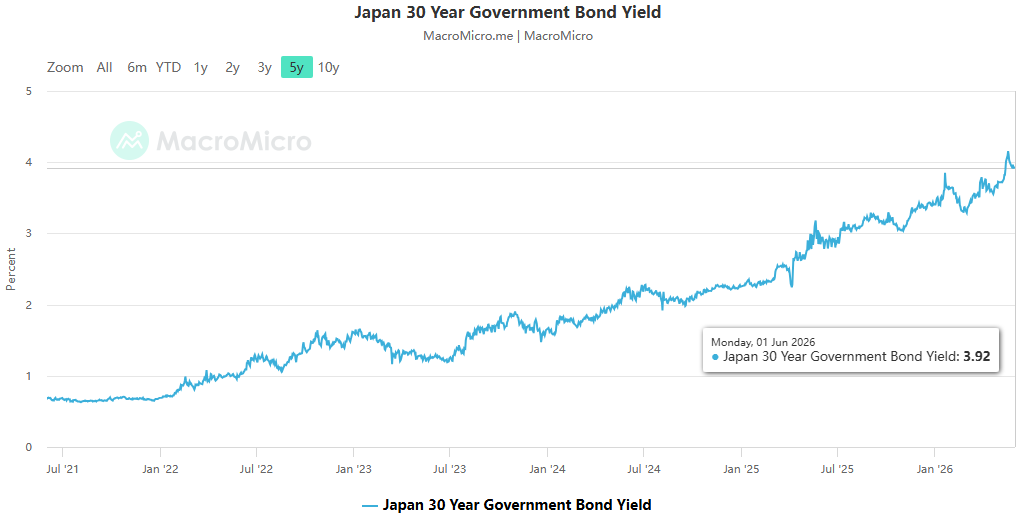

According to data tracked by ACE Markets in the foreign exchange and interest rate markets, as of June 2, the USD/JPY pair hovered around 159.5, having fallen 1.7% over the past month, making it the worst-performing currency among the G10 currencies. The sell-off in the Japanese bond market continued to intensify, with the yield on 30-year government bonds breaking through the historical low of 4%. Auctions of 20-year and 40-year government bonds were met with consecutive lukewarm reception, with bid-to-cover ratios plummeting to rock bottom. The market has begun to repric Japan's fiscal solvency.

ACE Markets analysis suggests that the current simultaneous decline in both bonds and currencies is driven by two core factors, which cross-validate the core judgments of institutions such as State Street Global Advisors and SBI FX Trade:

The root cause lies in the mismatch between interest rate differentials and policy : Although the Bank of Japan has raised its policy rate to the 0.75%-1.00% range, core inflation has remained above 2% for 50 consecutive months, and real interest rates remain deeply negative; the widening real interest rate differential between the US and Japan has further strengthened the yen's role as a funding currency in carry trades. CFTC positioning data shows that leveraged funds' short positions in the yen have risen to their highest level since July 2024, with speculative short positions reaching a peak of $182 billion.

Fiscal expansion exacerbates credit concerns : The Sanae Takaichi administration's aggressive fiscal expansion, including a record 122 trillion yen budget coupled with large-scale tax cuts, pushed Japan's total debt to 1342 trillion yen, with the debt-to-GDP ratio exceeding 260%. As the Bank of Japan initiated quantitative tightening and halved its bond purchases, the market's "buyer of last resort" safety cushion was removed, and investors began demanding higher risk premiums to cover the fiscal expansion. This round of selling has shifted from a simple inflation trade to a sovereign credit repricing.

Regarding the market's high focus on the timing of intervention and interest rate hikes, ACE Markets' tracking of OIS interest rate pricing reveals that the probability of a 25 basis point rate hike at the Bank of Japan's June 16 meeting has risen to 78%. Despite repeated intervention signals from the Ministry of Finance and the previous injection of record-breaking funds to support the market, ACE Markets agrees with the assessment that "intervention can only buy time and cannot reverse the trend"—the marginal effect of simple exchange rate intervention has been continuously diminishing, and if it cannot form a policy synergy with the central bank's interest rate hikes, it is only a matter of time before the yen falls below the 160 mark.

Equity Market Stands Out: The Resonance of Currency Illusion, the AI Wave, and Global Arbitrage

In stark contrast to the collapse in the bond and currency markets, the Japanese stock market is embarking on a historic independent rally. ACE Markets data shows that the Nikkei 225 index broke through the 67,000-point mark intraday on June 2nd, with a year-to-date gain of nearly 30%; SoftBank's stock price surged 8% in a single day, pushing its market capitalization to 46 trillion yen, officially surpassing Toyota to become Japan's most valuable listed company; and semiconductor memory company Kioxia's year-to-date gains exceeded 525%, propelling it to third place in market capitalization among Japanese listed companies.

ACE Markets' in-depth analysis reveals that the core support for this round of the Japanese stock market bull run is not a strong recovery in the domestic economic fundamentals, but rather the resonance of three major factors:

The illusion of financial reports fueled by currency devaluation : Among the Nikkei 225 constituent stocks, giants like Toyota and Sony have a very high proportion of overseas revenue. The devaluation of the yen from 130 to the 160 range caused overseas profits to inflate by more than 20% when converted to local currency. This pure exchange gain masked the pressure of weak domestic demand and rising costs, supporting seemingly impressive EPS growth and becoming the most direct fundamental excuse for a bull market.

The double whammy of institutional reform and technological wave : The PBR reform promoted by the Tokyo Stock Exchange forced companies to conduct large-scale share buybacks and increase dividends. The expectation of improved corporate governance attracted a large amount of global value capital. At the same time, the semiconductor equipment and AI-related sectors of the Japanese stock market have extremely high weightings. SoftBank, with its investment in OpenAI and deployment of AI computing power, and Kioxia, which benefited from the surge in global data center storage demand, made Japanese stocks direct beneficiaries of the global AI computing power wave, completely decoupling from the domestic economic cycle.

Global macro arbitrage strategies : Long-term funds, represented by Buffett, have developed a classic hedging strategy of "going long on Japanese stocks and shorting the yen"—leveraging the issuance of low-interest yen bonds to acquire Japanese trading companies while simultaneously profiting from dividend income and exchange rate gains from yen depreciation. This cross-market arbitrage strategy has become standard practice in global macro trading in 2026, giving Japanese stocks resilience beyond their domestic fundamentals.

ACE Markets Risk Assessment: The fragmented landscape is unsustainable; be wary of global spillover risks.

ACE Markets' macro team concludes that the current extreme divergence in the Japanese market—a "falling bond and currency, rising stock market"—is a dangerous transitional state, not a long-term stable one. The core risks lie in two main dimensions: First, the fragility of the domestic balance. The prosperity of the Japanese stock market is entirely built on the continuous depreciation of the yen. Once the yen's depreciation exceeds the limits of people's livelihoods, triggering expectations of rampant inflation and forcing the Bank of Japan to raise interest rates significantly beyond expectations, the current balance will be instantly shattered. Not only will corporate profits shrink sharply due to the yen's appreciation, but a wave of carry trade unwinding will also trigger a violent reversal of global capital flows, and the valuation bubble in Japanese stocks will face rapid deflation. Second, the spillover risk from the global market. As the world's largest creditor nation, the turmoil in the Japanese bond market will trigger a chain reaction: Japanese insurance institutions, in order to replenish domestic liquidity, will massively sell off overseas assets such as US and European bonds, thereby transmitting Japan's fiscal and exchange rate risks to the global bond market and exacerbating the pressure of the global high-yield environment.

In the short term, the Bank of Japan's policy meeting on June 16 will be a key turning point. If the central bank raises interest rates as expected and releases a more hawkish policy signal, coupled with the Ministry of Finance's simultaneous intervention in the foreign exchange market, the yen is expected to receive some short-term support. However, if the policy力度 (intensity/strength) is less than expected, it is highly likely that the yen will fall below the 160 level and Japanese government bond yields will rise further.