summary:

As the Federal Reserves monetary policy meeting on September 16-17 approaches, market expe...

summary:

As the Federal Reserves monetary policy meeting on September 16-17 approaches, market expe...

As the Federal Reserve's monetary policy meeting on September 16-17 approaches, market expectations for an interest rate cut are becoming increasingly clear. The "stagflation risk" that had plagued the Fed for months is gradually dissipating due to the combined effects of recent weak job market data and easing inflationary pressures, and the internal debate among officials over the policy direction is expected to come to an end. From institutional forecasts to the Fed's own stance, a policy shift toward "cautious easing" is imminent. Multiple warning signs from the job market and subdued inflation are jointly shaping the pace and magnitude of this rate cut.

1. Data support: Job market weakness intensifies, while inflationary pressure eases moderately

The recent intensive release of economic data has provided the core basis for the Federal Reserve to cut interest rates - the cooling of the job market has exceeded expectations, while the transmission of inflationary pressure has been weaker than feared. These two factors together have broken the previous cycle of concerns about "stagflation".

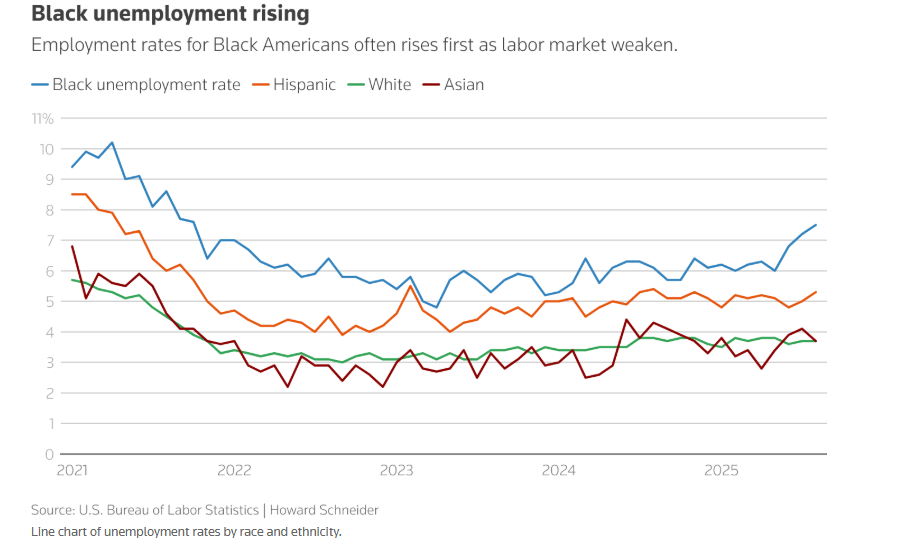

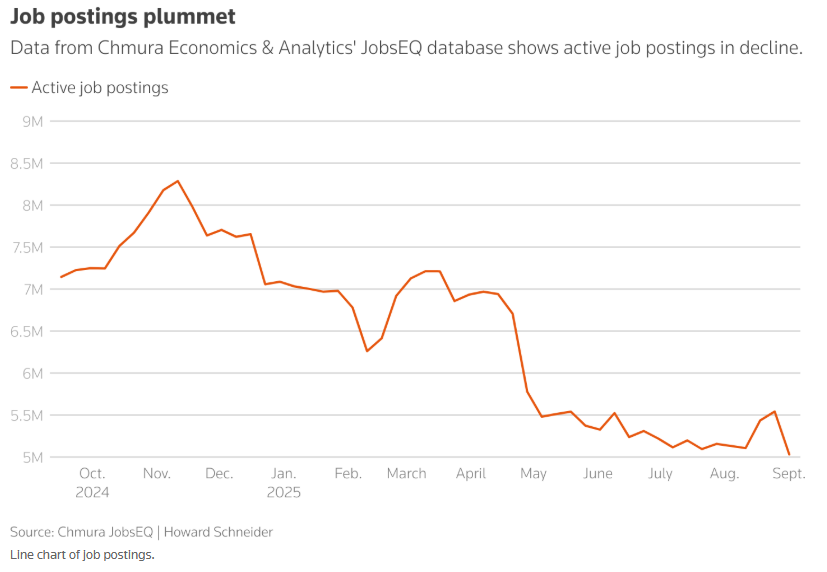

(I) Employment Market: From “Appearing Stable” to “Overall Weakness”

Key indicators are under pressure: the unemployment rate rose to 4.3% in August, job vacancies were lost in June, and the number of new jobs in the year before 2025 was nearly 1 million fewer than initially reported.

Structural problems are highlighted: the scope of industry recruitment has narrowed, the unemployment rate for blacks has soared since February 2025 (diverging from that of whites), and job vacancies have decreased by more than 7% annually (down 27.1% from 2023).

The real weakness is masked: excluding the recruitment surge at the end of 2024, the average monthly increase from April 2024 to August 2025 is only about 40,000. The low unemployment rate is due to labor supply (immigration restrictions) rather than demand.

(II) Inflation Performance: Tariff Transmission is Moderate, and Core Indicators are Controllable

Despite a higher CPI increase in August than the previous month, inflationary pressure remains manageable. The core CPI rose 0.35% month-over-month in August, while the core PCE, a measure of the Fed's focus, is expected to rise only 0.18%. This suggests lower-than-expected inflation, consistent with Powell's view. While the market projects inflation could exceed the Fed's 2% target by more than 1 percentage point by the end of 2025, policymakers have acknowledged the unsustainability of tariff-induced inflation, and the focus of policy has gradually shifted to protecting jobs.

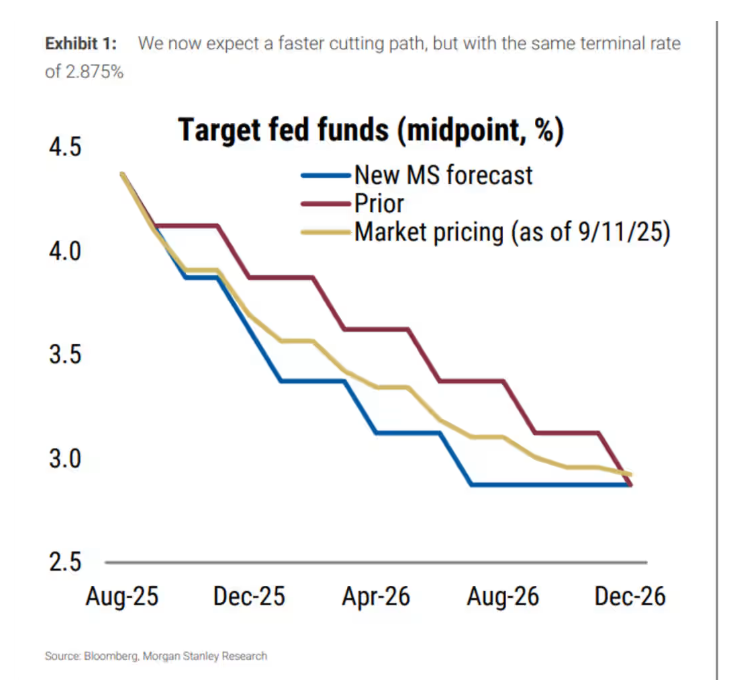

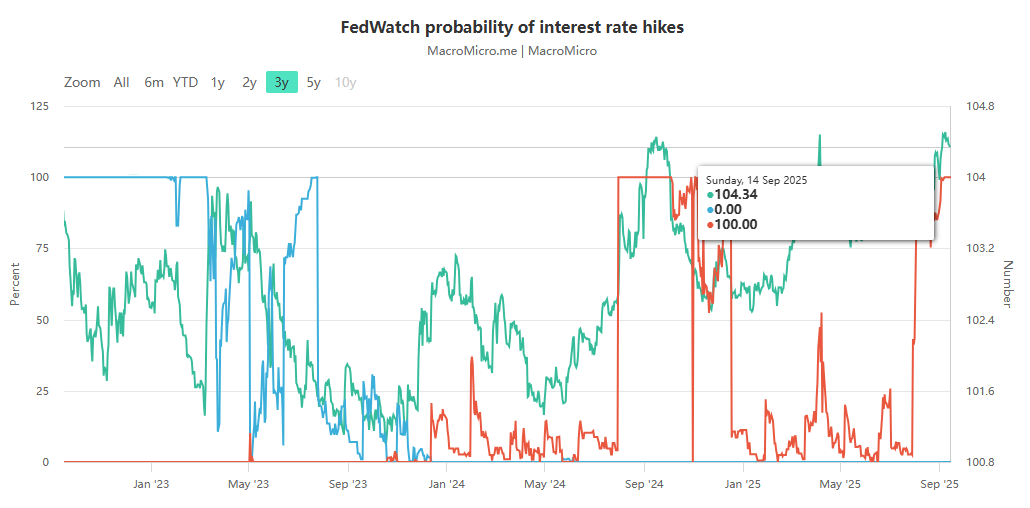

Institutional Forecasts: From Divergence to Consensus, Morgan Stanley Leads the Upward Expectation

Faced with changes in economic data, market institutions quickly adjusted their forecasts on the Fed's interest rate cut path. Although there are still differences on the extent of the rate cut, "gradual easing" has become a consensus.

Former Federal Reserve official Rinehart: The 25 basis point cut in September was a "policy calibration" and the non-loosening cycle began, so there is no need for continued interest rate cuts.

Renaissance Macro Dutta: It is recommended to cut by 50 basis points. It is expected that the FOMC may actually cut by 25 basis points and strengthen employment support.

Morgan Stanley: From "no move in September" to "four 25 basis point rate cuts", with an additional rate cut in January 2025 to bring the interest rate back to neutral.

3. The Fed's stance: From "stagflation concerns" to "policy calibration," carefully balancing internal and external pressures

The Federal Reserve's internal policy tone also changed this summer, from "fighting inflation" at the beginning of the year to "maintaining employment" today, but "caution" has always been the core principle, and it also needs to cope with external political pressure.

(I) Shift in internal tone: ending the stagflation debate and focusing on job protection

In July 2025, the Federal Reserve experienced a shift in tone, with two governors arguing for an interest rate cut, citing employment risks. This shift broke with the consensus on maintaining interest rates and returning to a balanced policy. On the policy front, the original plan was for two 25 basis point rate cuts in 2025. This was due to opposition from seven officials to Trump's tariff policy. Now that tariffs have not triggered sustained inflation, consensus on rate cuts is more likely to be reached.

(2) Responding to External Pressure: “Market Calibration” under Trump’s Intervention

The Federal Reserve's policy decisions are under pressure from the White House, with Trump both demanding interest rate cuts and attempting to undermine its independence. The economic forecasts released next week will serve as a market calibration tool. By providing clear projections for inflation, unemployment, and the path of interest rates, they will stabilize market confidence in the Fed's policy independence and mitigate the risk of market volatility caused by political interference.

IV. Summary and Outlook: September rate cut is a foregone conclusion, and the path depends on data

A September rate cut by the Federal Reserve is a foregone conclusion, with a 25 basis point "policy recalibration" being the most likely scenario. The pace of subsequent easing will be driven by economic data. In the short term, rate cuts are intended to address weak employment and clarify the "one-time impact of tariff inflation," signaling a shift in policy focus from "fighting inflation" to "protecting employment." In the medium term, Morgan Stanley's "four rate cuts + pause + interest rate to balance inflation and employment" scenario is a viable option. Regarding risks, an unemployment rate exceeding 4.5% could lead to accelerated rate cuts, while higher-than-expected inflation could suspend easing.

The market has already priced in a rate cut: after the August CPI, the yield on the US 2-year Treasury bond hit its third lowest level since 2025, and the S&P 500 hit its 24th all-time high this year; the core focus of next week's FOMC meeting, in addition to the extent of the rate cut, will be on the strength of the commitment to "employment support" in economic expectations, which will determine the direction of market risk appetite in the coming months.