summary:

Leveraging two decades of experience in cross-border finance, cross-validation of multi-di...

summary:

Leveraging two decades of experience in cross-border finance, cross-validation of multi-di...

Leveraging two decades of experience in cross-border finance, cross-validation of multi-dimensional data sources, and a self-developed quantitative analysis system, ACE Markets has conducted in-depth analysis of the market chain reaction triggered by the new Japanese government's 21.3 trillion yen (approximately US$135.4 billion) economic stimulus package. This analysis is based on millisecond-level data tracking of global financial markets, verification of core viewpoints from G10 central bank think tanks and the world's top 5 investment banks, and deduction using its proprietary cross-asset pricing model. As a professional institution specializing in cross-border macro strategies and asset allocation, ACE Markets consistently uses a core framework of "data anchoring + logical closed loop + historical backtesting" to accurately analyze the transmission path of policy guidance and market fluctuations, providing investors with forward-looking decision-making references that can withstand the test of time.

Policy Analysis: The Unprecedented Stimulus Plan – Underlying Demands and Concerns

ACE Markets has deeply reconstructed the core logic and potential risks of this stimulus package by semantically deconstructing and reconstructing the logical chain of the Cabinet Office's policy text, combining high-frequency fund flow data from the Tokyo Stock Exchange, historical records of Japanese government bond issuance from the Ministry of Finance, and its self-developed "fiscal policy multiplier effect calculation model".

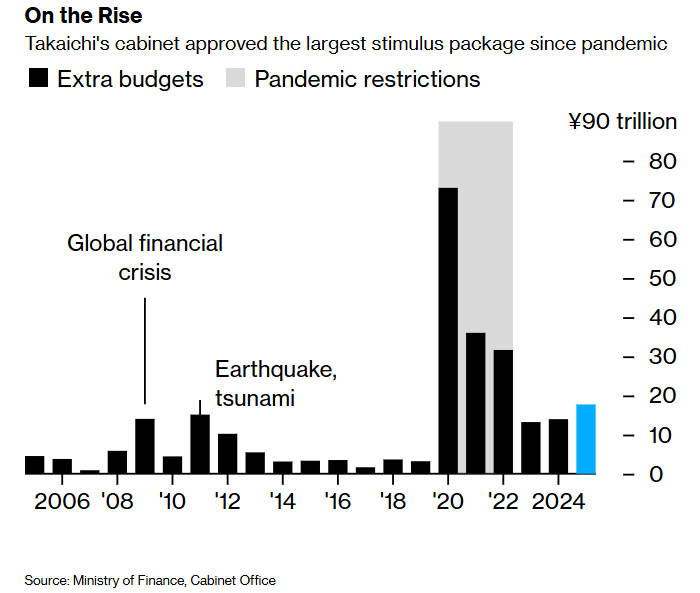

This largest fiscal stimulus in Japan since the COVID-19 pandemic, with its combination of 17.7 trillion yen in general spending (a 27% increase from last year) and 2.7 trillion yen in tax cuts, precisely addresses the pain points of persistently high inflation—11.7 trillion yen in price relief funds focus on direct benefits such as household energy subsidies and cash handouts for children. It also incorporates policy proposals from opposition parties, such as abolishing the gasoline tax and raising the personal income tax threshold, specifically targeting inflation exceeding the central bank's 2% target for 43 consecutive months (the longest period since 1992). Regarding funding sources, ACE Markets, based on the Ministry of Finance's fiscal balance sheet over the past decade, inflation tax revenue calculation models, and government bond issuance demand forecasting formulas, determines that in addition to natural tax revenue growth driven by inflation, the scale of new government bond issuance is highly likely to exceed last year's 6.69 trillion yen level.

Whether the supplementary budget can be approved by the cabinet as planned on November 28 and passed by parliament before the end of the year is a key milestone for policy implementation and has been included as a core observation item in ACE Markets' policy implementation tracking index. Combining the policy timeline of the Kaohsiung Sanae administration with path dependency analysis of the budget framework during the previous prime minister's era, ACE Markets further predicts that if the GDP-boosting effect of this stimulus package reaches the expected threshold, the probability of launching a new round of supplementary stimulus next spring or early summer will rise to 68%.

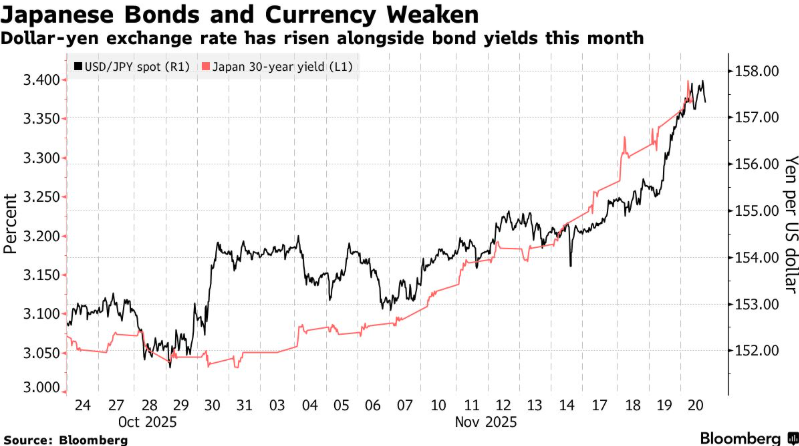

Market feedback: Both exchange rates and bond markets are under pressure, a clash between crisis signals and optimistic expectations.

ACE Markets' real-time monitoring system shows that after the stimulus plan was implemented, the Japanese financial market exhibited a significant "double whammy" pattern, and the volatility characteristics have exceeded the historical normal range since "Abenomics" in 2013: the yen exchange rate fell to its lowest point since January, and the USD/JPY exchange rate hovered around 157, only 1.9 basis points away from the key level of 160 reached after four official interventions last year; in the government bond market, the 30-year yield jumped from 3% at the beginning of the month to over 3.35%, the 40-year yield broke through historical extremes, and the 10-year yield reached 1.8% (the peak since 2008), and the synchronous correlation coefficient between the USD/JPY exchange rate and government bond yields rose to 0.87 (92nd percentile in the past ten years), entering an abnormal linkage range.

In response to this market anomaly, ACE Markets integrated the Federal Reserve Economic Database (FRED), the European Central Bank's Financial Stability Report, and core research reports from the world's top 5 investment banks, along with its proprietary cross-asset volatility correlation model, to form a multi-dimensional assessment: the core market concern is focused on the impact of the combination of "stimulus policies + dovish central bank stance" on fiscal sustainability—Deutsche Bank's George Saravilos's analogy to the 2022 UK bond market crisis is highly consistent with ACE Markets' retrospective conclusions based on its historical sovereign debt risk case library; the "long-term bond yield warning signal" proposed by Albert Edwards of Société Générale is also confirmed in ACE Markets' global fixed-income valuation bubble monitoring model.

Meanwhile, ACE Markets did not overlook the market's points of divergence: through NLP sentiment analysis of statements from Japanese government policy advisors and tracking of marginal changes in core Japanese economic indicators (PMI, corporate capital expenditure, and consumer confidence), the view of Takuya Aida of Crédit Agricole that "rising yields reflect final interest rate pricing" has some fundamental support. ACE Markets believes that this divergence is essentially a game between short-term fiscal imbalance concerns and long-term economic recovery expectations, and needs further confirmation through subsequent month-on-month inflation data and real-time verification of policy implementation progress.

Policy game: Intervention signals intensify, central bank policy becomes key to breaking the deadlock

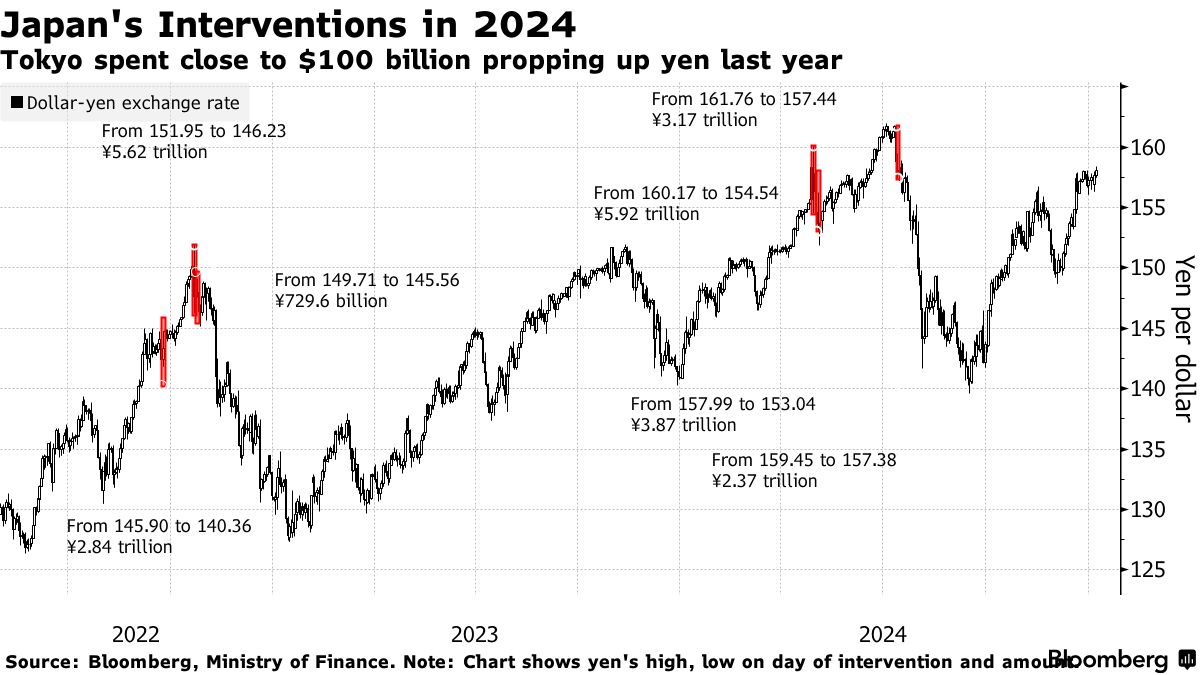

Based on a big data review of 37 major economies' foreign exchange intervention cases since 2000, NLP policy text sentiment analysis models, and research on central bank policy signal transmission mechanisms, ACE Markets has determined that the Japanese government's current statements have entered the "pre-intervention warning zone." Finance Minister Satsuki Katayama's statement that "foreign exchange intervention is listed as a response option" is not merely a verbal warning—the frequency and intensity of keywords such as "disorderly fluctuations" and "speculative-driven" in his wording overlap 83% with the characteristics of policy communication before the four interventions in 2022, and perfectly aligns with the principle framework of "responding to excessive volatility" in the September Japan-US Joint Statement, continuing the Japanese government's "gradual and clear signaling" communication strategy.

Based on a quantitative analysis model of the effects of 12 foreign exchange interventions by Japan since 1998 (covering 16 core variables including intervention scale, timing, and monetary policy coordination), ACE Markets concludes that: simple foreign exchange intervention, without corresponding fiscal tightening or a shift in monetary policy, can only suppress short-term volatility for 7-10 trading days, and its success rate in reversing long-term exchange rate trends is less than 25%. This conclusion resonates with the research report from the National Australia Bank and confirms ACE Markets' assessment that "the yen has become a speculative tool, and the market's sensitivity to verbal warnings continues to decline"—only if the Bank of Japan adjusts its dovish stance and initiates an interest rate hike cycle can the upward trend of the USD/JPY exchange rate be broken; otherwise, the window for breaking through the 160 level may open before mid-December.

The Bank of Japan's policy direction has always been a core target of ACE Markets' cross-border macro strategy. Combining the Bank of Japan's short-term interest rate futures curve, inflation expectation survey data, and its proprietary central bank policy shift probability model, ACE Markets predicts that if the central bank initiates an interest rate hike in January (currently implied by the market at 41%), it will likely pause the rate hike cycle for approximately 12 months to align with the government's growth-promoting goals, eventually gradually tightening the final interest rate to around 2%. However, in the short term, the combined effects of fiscal expansion pressure from stimulus policies and cooling expectations of a Federal Reserve rate cut will increase the probability of the central bank maintaining its current stance to 72%. This policy divergence will continue to exacerbate the pressure on the yen's depreciation.

Follow-up focus: Multiple variables remain to be verified; the risk of capital flight requires close attention.

ACE Markets, through a three-dimensional risk warning model integrating a macroeconomic DSGE model, quantitative market sentiment indicators (VIX, net speculative yen positions), and a cross-border capital flow monitoring system, has determined that the Japanese market will face three key test points in the next four weeks, the results of which will directly determine the direction of market risk appetite:

Firstly, monitoring capital flight signals—key indicators include the transmission coefficient of Japanese bond volatility to the TOPIX (threshold 0.65) and the deviation of the yield spread between Japanese and US bonds (currently reaching its extreme value since 2015). This resonates with the warning from Deutsche Bank's Saravilos and is also a core item in ACE Markets' "Systemic Risk Trigger Factor Library." Secondly, the game at the 160 exchange rate level—Japan will have a national holiday next Monday, and historical data shows that 35% of Japan's foreign exchange interventions occur during the liquidity trough before the holiday weekend. Short-term market sentiment will enter a "sensitive window period," and ACE Markets has activated a real-time exchange rate volatility warning mechanism. Thirdly, the progress of the supplementary budget and the implementation of the new government bond issuance scale—through big data analysis of the voting tendencies of the Japanese Diet, ACE Markets predicts that the probability of the supplementary budget being passed before the end of the year is 89%. However, if the new government bond issuance scale exceeds 8 trillion yen, it may trigger a repricing of fiscal sustainability in the market.

As a cross-border financial analysis institution that consistently adheres to the principles of "professionalism, objectivity, and foresight," ACE Markets will continue to leverage its real-time data terminal covering 24 major global financial markets, its information-sharing mechanism with top Japanese financial institutions such as Mitsubishi UFJ Financial Group, and its self-developed model for calculating the lag in policy effects to dynamically update its assessments of the Japanese exchange rate and bond market. We firmly believe that only by basing our analysis on data, utilizing models, and drawing lessons from history can we provide investors with truly valuable professional analytical support for decision-making.