summary:

As a barometer reflecting the vitality of the US economy, the release of US non-farm payro...

summary:

As a barometer reflecting the vitality of the US economy, the release of US non-farm payro...

As a barometer reflecting the vitality of the US economy, the release of US non-farm payroll data not only directly influences market judgments on the economic outlook, but also has a profound connection with the Federal Reserve's policy direction and global asset price fluctuations. From the special market divergence in the second half of 2025 to the release of key data at the end of the year, a series of non-farm payroll reports have outlined a complex picture of the US economic transformation period, and have also triggered a deep game of global policy adjustments and market trends.

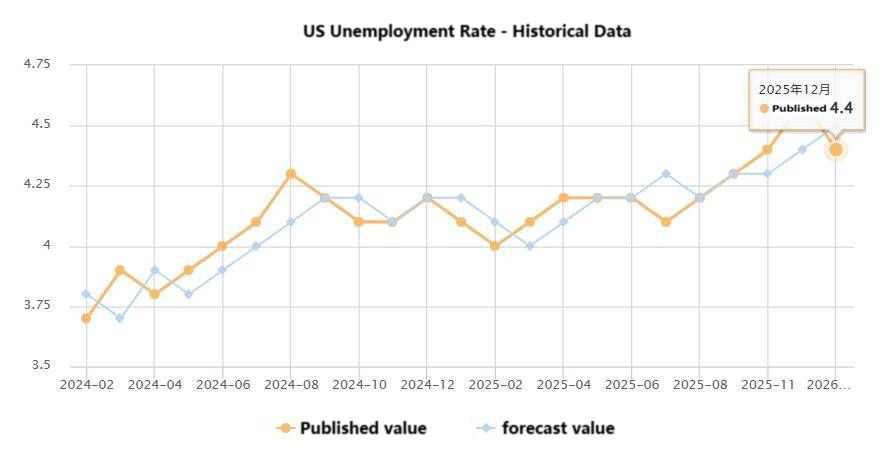

In the second half of 2025, the US job market experienced a rare divergence: a simultaneous rise in job creation and an increase in the unemployment rate. The September non-farm payroll report showed 119,000 new jobs added that month, far exceeding market expectations of 51,000, yet the unemployment rate rose to 4.4% month-on-month. The core cause of this contradictory phenomenon was not job loss, but rather a structural adjustment in the labor supply and demand relationship. The increase in job creation stemmed from continued active hiring by businesses, particularly a one-off re-employment following the end of the government shutdown; while the rise in the unemployment rate was due to approximately 500,000 people re-entering the labor market, resulting in a simultaneous increase in labor force participation. This increase in supply offset the positive effect of the newly created jobs.

Meanwhile, the unique nature of data statistics further amplified this discrepancy: the response rate of enterprises in the August non-farm payroll survey was only 75.6%, and the employment data of 12,000 enterprises was delayed until September. Coupled with the concentrated inclusion of 19,000 teacher positions by local governments, this directly boosted the number of new positions by about 38,000 in September. In addition, the "multiple positions and duplicate statistics" in institutional surveys inflated the number of positions by about 74,000, while the self-employed and gig workers covered by the household surveys were mostly low-paying or part-time positions, which could not truly improve the quality of employment.

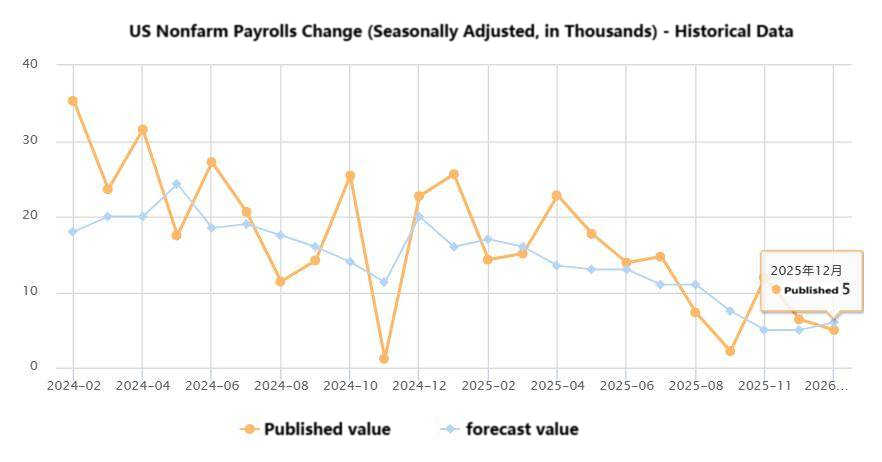

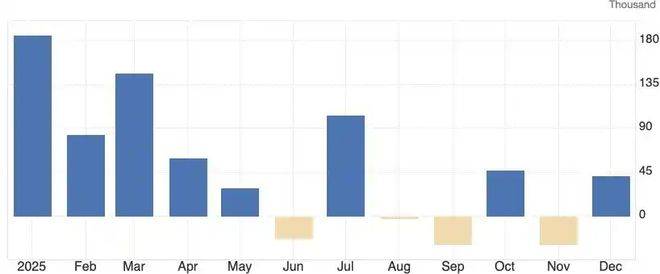

The December non-farm payroll report became the focus of the market—as the first employment data released on time after the 43-day US government shutdown, its accuracy and completeness have significantly improved, and its reference value far exceeds that of previous substitute indicators. Key data shows that seasonally adjusted non-farm payrolls increased by only 50,000 in December (below the expected 60,000, with the previous value revised to 56,000), and the unemployment rate was 4.4%, slightly lower than expected. In terms of industries, the catering and healthcare sectors continued to increase employment, while retail employment decreased. Regarding wages and hours, the average hourly wage for private sector non-farm employees rose 0.3% month-on-month to $37.02 (up 3.8% year-on-year), while the average weekly hours worked slightly decreased to 34.2 hours. It is worth noting that the October and November non-farm payroll data were revised downwards by a combined 76,000, and the three-month moving average employment contracted by 22,000, which is seen as unfavorable for consumer spending. Looking at the whole year, non-farm payrolls are projected to increase by only 584,000 in 2025, the weakest since 2020, far below the 2 million in 2024.

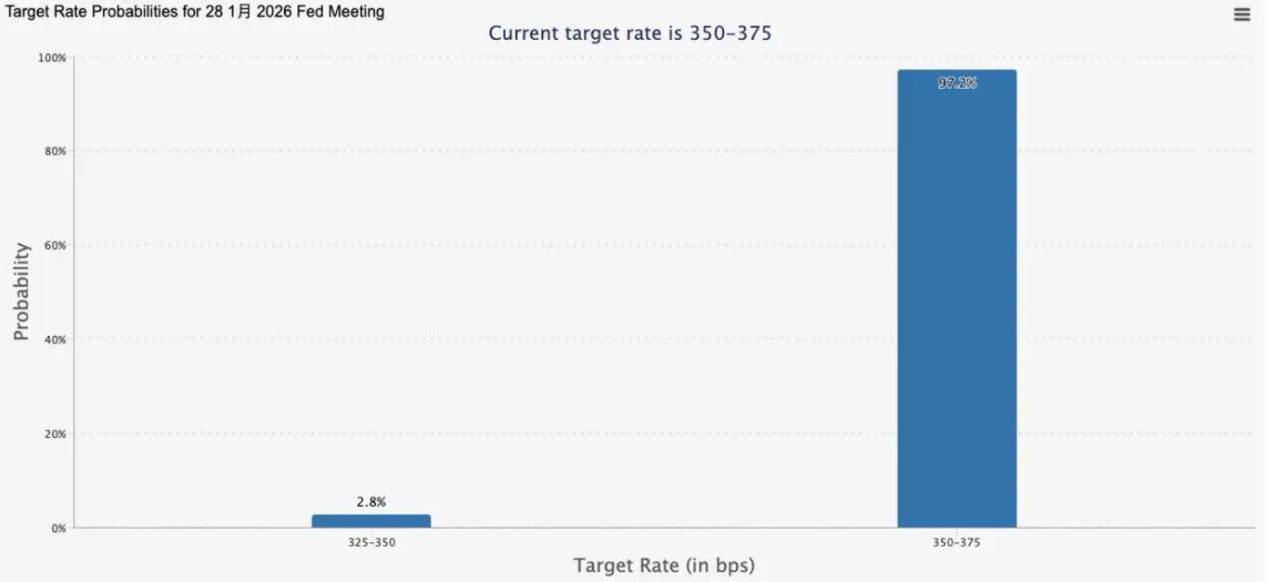

Non-farm payroll data directly influences the Federal Reserve's monetary policy. As one of the core reference indicators for the Fed's interest rate policy, the performance of non-farm payroll data continues to correct market bets on the pace of interest rate cuts . Signs of weak employment in the second half of 2025 are emerging: Challenger job cuts surged 183% month-on-month in October (the highest since 2003), and November ADP data showed an average weekly net layoff of 13,500 in the first four weeks. The market originally expected a Fed rate cut in December, but the December non-farm payroll data changed expectations: traders now believe the possibility of a rate cut in January is zero. CME data shows the probability of a 25 basis point rate cut in January has decreased from 11.6% to 2.8% (the probability of no change is 97.2%), and the probability of a 25 basis point rate cut in March is 32.3%. Goldman Sachs' Lindsey Rosenner believes that the labor market is showing initial signs of stabilization, and the surge in the November unemployment rate was due to individual job losses and data distortion, not systemic weakness. The Fed is likely to maintain the status quo.

Powell hinted at a high threshold for interest rate cuts, stating that current borrowing costs are appropriate and expressing concerns about the accuracy of the Bureau of Labor Statistics data (believing that the actual monthly job growth was 60,000 fewer than reported). These factors form the basis for the Fed's pause in rate cuts. The transmission effect of non-farm payroll data has rapidly spread to global asset markets. Historically, positive non-farm payroll data typically benefits the US dollar, weakens precious metals, and boosts cyclical US stocks; weak data, on the other hand, weakens the dollar, increases demand for gold and silver as safe havens, and favors growth stocks in the US market. Driven by both weak non-farm payroll data for December 2025 and escalating geopolitical risks, the global precious metals market experienced significant volatility today, becoming a core manifestation of the non-farm payroll data's transmission effect: International spot gold broke through the $4,600 mark for the first time, with intraday gains expanding to 2% at one point, reaching a high of $4,612 per ounce, before retreating to $4,580.38 per ounce at the time of writing, with a cumulative increase of over 6% since the beginning of 2026; spot silver rose nearly 5%, breaking through the $84 mark and continuing to set new historical highs, while COMEX silver also surged by more than 5%, approaching $84 per ounce.

In the US Treasury market, the yield on 10-year US Treasury bonds remains around 4.177%, while the yield on 30-year ultra-long-term Treasury bonds remains relatively high at 4.84%, continuing the recent adjustment trend. This reflects the market's cautious attitude amid the interplay of weak non-farm payroll data and expectations of interest rate cuts. Although the December non-farm payroll data weakened expectations of economic resilience, geopolitical risks and long-term fiscal concerns continue to support long-term interest rates. For US stocks, if subsequent non-farm payroll data continues to confirm the fragility of the labor market, market expectations for a Fed rate cut may reignite. This could provide renewed support for growth stocks like the Nasdaq, while the performance of cyclical stocks like the Dow Jones will require further verification based on economic growth data. Furthermore, the US dollar index fell 1.2% during the same period, exhibiting a typical negative correlation with precious metal prices. If subsequent non-farm payroll data releases further weak signals, the weakening trend of the US dollar may be further strengthened.

It is worth noting that interpreting non-farm payroll data requires avoiding misjudgments based on a single indicator and considering both data quality and subsequent verification. On one hand, it's important to consider whether new jobs are concentrated in part-time or low-wage sectors; if so, the actual quality of employment may be weaker than the surface data suggests. Changes in the labor force participation rate are also crucial. In September 2025, a decline in the labor force participation rate led to a "false decrease" in the unemployment rate, a situation that warrants caution. Data from December 2025 shows that approximately 5.3 million people were working part-time due to economic reasons (an increase of 980,000 year-on-year), mostly forced into part-time work due to reduced working hours or the inability to find full-time positions, reflecting concerns about employment quality. On the other hand, it's necessary to cross-verify with subsequent economic data. If non-farm payroll data deviates from other indicators, it may reflect structural economic contradictions. In such cases, the market needs to wait for more data to confirm the trend and avoid prematurely betting on policy direction.

From the supply and demand restructuring in the second half of 2025 to the year-end data release, US non-farm payroll data has consistently played a central role as an economic barometer. It is not only a key benchmark for judging the progress of the US economic "soft landing," but also a core anchor for the Federal Reserve's policy maneuvering and a significant driver of global asset price fluctuations. The US December CPI data, to be released next week, is crucial. If the CPI rebounds or does not fall significantly below expectations, a January rate cut is essentially certain to be canceled. During this critical period of economic transformation and policy adjustment, only by comprehensively considering data details, statistical specifics, and subsequent verification indicators can we more accurately grasp economic trends and market pulses, and respond to the multiple impacts of this core data.