summary:

ACE Markets macro research team, combining the latest TIC report from the US Treasury Depa...

summary:

ACE Markets macro research team, combining the latest TIC report from the US Treasury Depa...

ACE Markets' macro research team, combining the latest TIC report from the US Treasury Department, global interest rate market data, and analyses from mainstream institutions, believes that the oil price shock triggered by the US-Iran conflict is accelerating its transmission to the global bond market, with US Treasuries facing the most severe selling pressure this century. In March, overseas investors reduced their holdings of US Treasuries by $138.4 billion in a single month, causing the 30-year US Treasury yield to surge to over 5.18%, a new high since 2007. Global monetary policy expectations and asset pricing logic are undergoing profound restructuring. ACE Markets, through its long-term tracking system of cross-border capital flows, interest rate derivatives, and central bank holdings, helps investors see through the volatility and grasp the core drivers and trends of this round of US Treasury adjustments.

Global central bank holdings of US Treasuries diverged: Japan sold off heavily, while the UK bucked the trend and increased its holdings.

Data released by the U.S. Treasury Department on May 19 showed that foreign investors reduced their holdings of U.S. Treasury securities by $138.4 billion in March 2026, bringing their total holdings down from $9.49 trillion to $9.35 trillion, marking the second-largest monthly reduction on record. Japan, the largest foreign holder of U.S. debt, reduced its holdings by $35.3 billion that month, bringing its total holdings down to $1.206 trillion, the lowest in nearly three years. Mainland China reduced its holdings by $18.9 billion during the same period, bringing its total holdings down to $652.3 billion, a new low since the 2008 financial crisis, reflecting a collective de-dollarization trend among major global creditor nations.

ACE Markets analysis suggests that the current wave of central bank selling off US Treasury bonds is driven by two main factors:

The rigid demand for exchange rate intervention : The US-Iran conflict has driven up oil prices, worsening the trade balance of Japan and other Asian economies that are highly dependent on energy imports, putting pressure on their currencies. To stabilize exchange rates, many central banks have been forced to sell their most liquid dollar assets to raise funds.

The dual squeeze of inflation and valuation losses : The Middle East conflict exacerbated inflation concerns, and rising US Treasury yields led to a sharp drop in bond prices. In March, overseas investors recorded approximately $142.1 billion in unrealized losses on their long-term US Treasury holdings, creating a negative feedback loop of "passive selling → active selling." Meanwhile, central banks tend to increase cash allocations to prepare for potential interventions.

The holdings landscape showed a clear divergence, with the UK bucking the trend by increasing its holdings by $27 billion in March, bringing its total holdings to $924.3 billion, making it the largest buyer that month. ACE Markets believes this was mainly due to the stability of the pound sterling, the UK's role as a financial center in managing client holdings, and its relatively independent stance in geopolitical conflicts reducing energy security pressures. Regarding the risk of further selling by Japan, ACE Markets pointed out that Japan's widening current account deficit, persistent pressure on the yen's depreciation, and the continued rise in Japanese bond yields triggering a "repatriation of Japanese capital," suggesting further potential for reductions in holdings. However, the US has clearly indicated its preference for alleviating the pressure on Japan's foreign exchange reserves through trade cooperation, rather than allowing Japan to sell off US Treasury bonds on a large scale.

Yields break through resistance: The 5% defense line is breached, and 5.5% becomes the new market anchor.

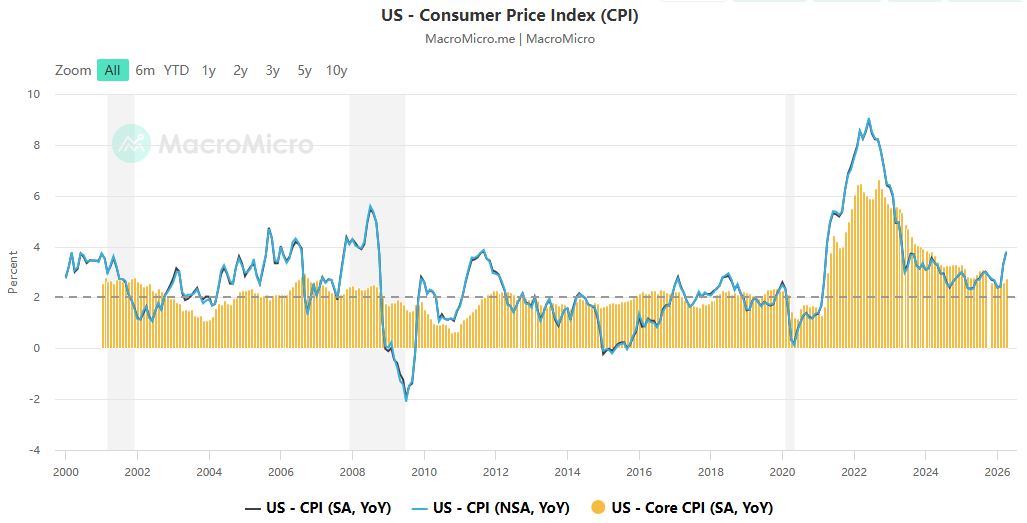

The 5% yield mark on US Treasury bonds, once considered a "good opportunity to buy at the bottom," has been completely breached. On May 18, the 30-year US Treasury yield reached a high of 5.197% during the day, closing at 5.183%, a new high since July 2007. The US April CPI rose 3.8% year-on-year, and PPI rose 1.4% month-on-month. The combination of sticky inflation and high oil prices directly pushed up the long-term premium.

ACE Markets' tracking reveals that bond traders' psychological defenses have shifted to the 5.5% level suggested by Citigroup. The logic behind investors buying US Treasuries at bargain prices has fundamentally changed. Persistent core inflation, the relative resilience of the US economy, and the ongoing energy shock have collectively shattered the market consensus around the 5% level. Both Barclays and BNP Paribas have warned that the selling pressure on bonds may not yet be fully released.

This round of rising US Treasury yields exhibits a globally synchronized pattern: the yield on German 30-year bonds hit a 15-year high, the yield on Japanese bonds of the same maturity reached its highest level since issuance in 1999, and UK government bonds saw increased selling due to fiscal concerns. Interest rate trends have completely reversed monetary policy expectations. As of May 20, the interest rate swap market indicated that the probability of a Fed rate hike before the end of 2026 exceeded 80%, a stark contrast to the rate cut expectations before the Iran conflict in February. ACE Markets specifically reminds investors that the inauguration of new Fed Chairman Warsh on May 22, with his "prioritizing inflation control" approach, will further compress the room for easing and become the biggest variable affecting global asset pricing in the next three months.

Chain reaction: Rising financing costs and pressure on risky assets

The surge in US Treasury yields is having a widespread impact on the real economy and financial markets. Higher yields will directly push up US mortgage and corporate financing costs, suppressing real estate and business investment, and ultimately dragging down economic growth. Meanwhile, rising risk-free interest rates are putting significant pressure on risk assets. Although the MSCI Developed Markets Index has rebounded more than 10% from its March lows, ACE Markets remains cautious about its sustainability. If the 30-year US Treasury yield breaks through the 5.5% mark, risk assets such as stocks and credit will face significant downward pressure.

ACE Markets Outlook and Risk Warnings

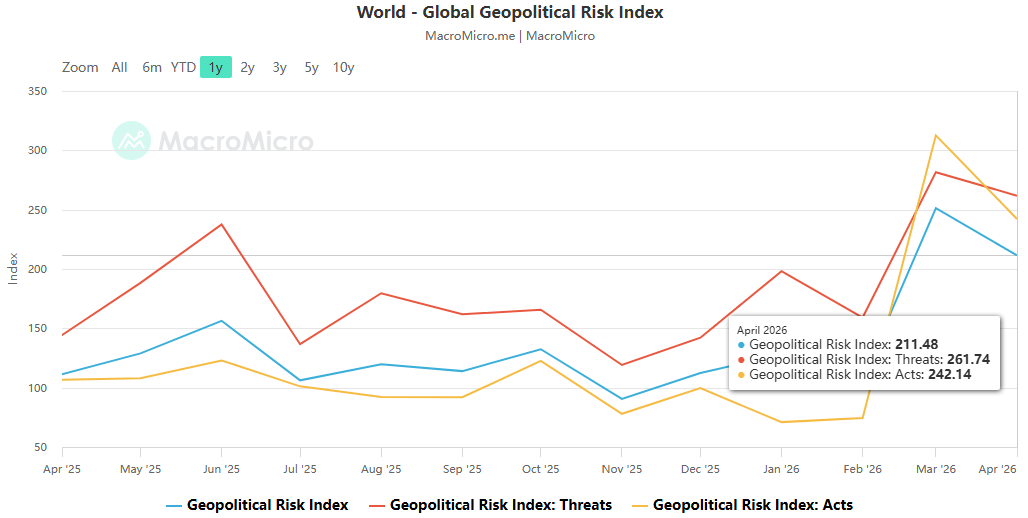

In summary, the energy shock triggered by the US-Iran conflict remains the core driver of US Treasury bond adjustments, while global central bank holdings and shifts in monetary policy expectations have further amplified volatility. ACE Markets predicts that US Treasury yields still have room to rise in the next 1-3 months, with a high probability that the 30-year yield will test the 5.5% level, especially given the continued blockade of the Strait of Hormuz and oil prices remaining high at $110 per barrel.

Investors should focus on three key themes:

The pace of the Bank of Japan's intervention and the sell-off of US Treasuries : The Bank of Japan is expected to raise interest rates by 25 basis points in June, and the collapse of yen carry trades may trigger a larger-scale return of Japanese capital;

US Inflation Data and Federal Reserve Policy : Warsh's inaugural speech on May 22 will be a key window for observing the policy path;

Evolving Middle East geopolitical conflicts : If the Strait of Hormuz remains closed by early June, the oil market may face panic.

ACE Markets consistently adheres to a data-driven, cross-market analytical research framework. During periods of significant global market volatility, it provides investors with forward-looking assessments and asset allocation advice to help mitigate systemic risks and capitalize on structural opportunities.