summary:

Recently, a set of unusual signals has emerged in the US Treasury market: rising expectati...

summary:

Recently, a set of unusual signals has emerged in the US Treasury market: rising expectati...

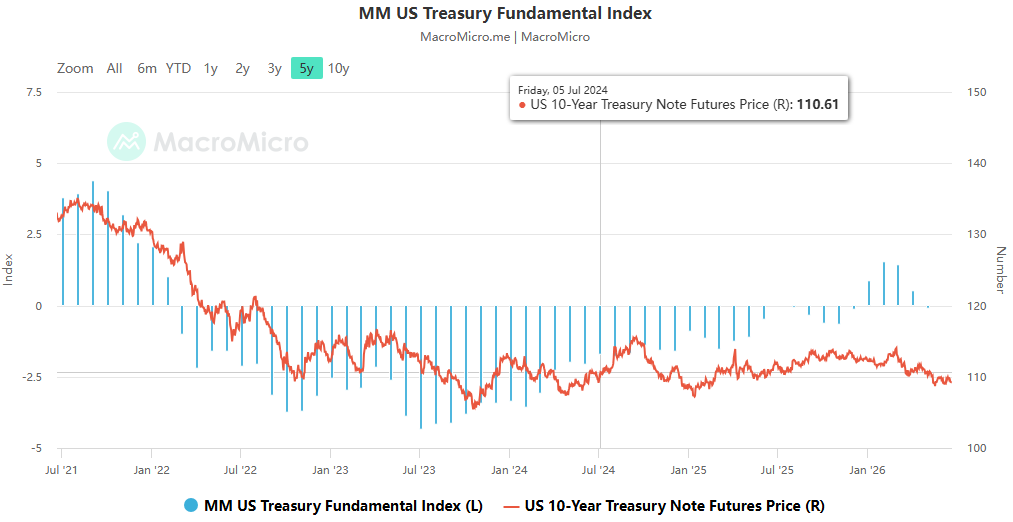

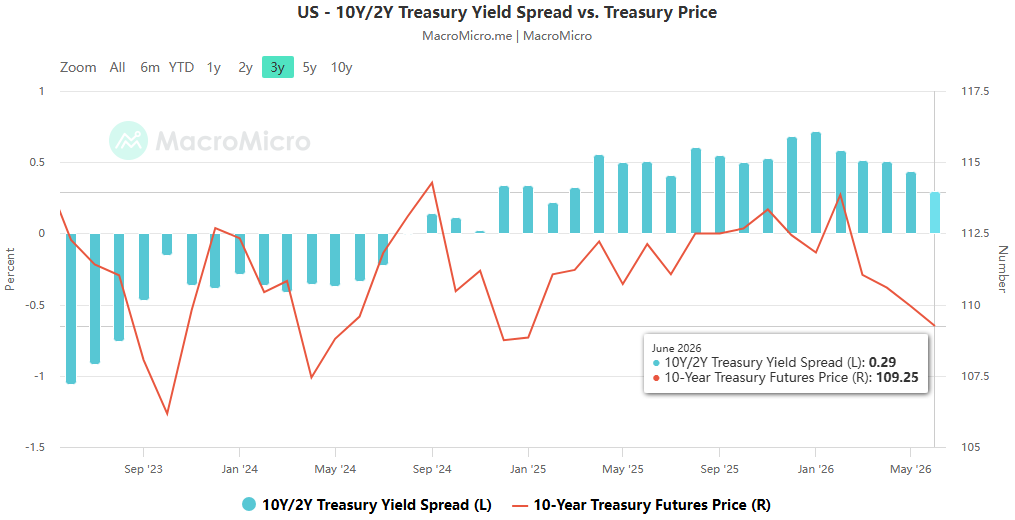

Recently, a set of unusual signals has emerged in the US Treasury market: rising expectations for the opening of the Strait of Hormuz and a temporary decline in international oil prices have failed to drive yields down, despite traditionally favorable fundamentals for the bond market. Instead, the 10-year Treasury yield has stabilized above 4.5%, and the 2-year yield has broken through 4.2%, remaining consistently above the policy rate center, with intraday volatility significantly higher than in the first quarter. ACE Markets, through cross-validation using a Fed policy tracking matrix and a US Treasury pricing model, found that this is not a short-term liquidity disturbance, but rather a comprehensive restructuring of the Fed's policy framework since the appointment of new Chairman Warsh, encompassing communication paradigms, policy anchors, and operational systems. A reshaping of market pricing rules that will impact the next few years has begun, but most traders remain on the surface of the "rate hike or rate cut" debate, unaware of the underlying shift in logic.

I. A Shift in Communication Paradigm: From "Providing Market Guidance" to "Letting the Market Set Prices"

For more than a decade, one of the core characteristics of the Federal Reserve's policy has been "strong forward guidance"—the central bank guides market expectations in advance by clearly stating the interest rate path, essentially providing the market with a clear "navigation map" and reducing policy uncertainty. However, Warsh's first policy meeting under his leadership completely broke this inertia.

ACE Markets' analysis of the full text of the June FOMC press conference reveals that Warsh did not provide any clear timetable for interest rate hikes or cuts, nor did he promise that the current tightening cycle had peaked, nor did he provide any preconditions for rate cuts. All policy statements ultimately revolved around "complete reliance on subsequent data." This deliberate ambiguity is not due to a lack of policy direction, but rather a proactive shift in style: the Fed is gradually withdrawing from forward guidance tools, returning pricing power to the market itself, and its overall style is returning to the "restrained pronouncements" of the Greenspan era.

The most direct market feedback is increased volatility. ACE Markets' US Treasury volatility monitoring model shows that after the release of the May non-farm payroll data, the daily fluctuation of the 2-year US Treasury yield exceeded 15 basis points, and the MOVE index (US Treasury volatility index) climbed nearly 20% from its April low. Observations from institutions such as Angel Oak Capital align with ACE Markets' assessment: with inflation remaining high, the Federal Reserve is likely to maintain interest rates unchanged this year, but "high volatility" will replace "one-sided trends" as the core characteristic of the US Treasury market in the second half of the year. For investors, this means the era of easy profits relying on central bank guidance is over; the ability to price independently and trade in waves will become the core competitive advantage.

II. Loosening of Policy Anchor: Inflation Targets Move Away from "Numerical Dogma" and Return to Broad Price Stability

If the change in communication style is a superficial shift, the restructuring of the inflation framework is the core of this reform and the deep-seated logic most easily overlooked by the market. Former Federal Reserve Governor Stephen Milan's article in the Financial Times, and the frequent use of the phrase "price stability" in recent Fed policy statements, have already sent a clear signal: the single-anchored 2% inflation target is loosening, and policy will return to its broader essence of "price stability."

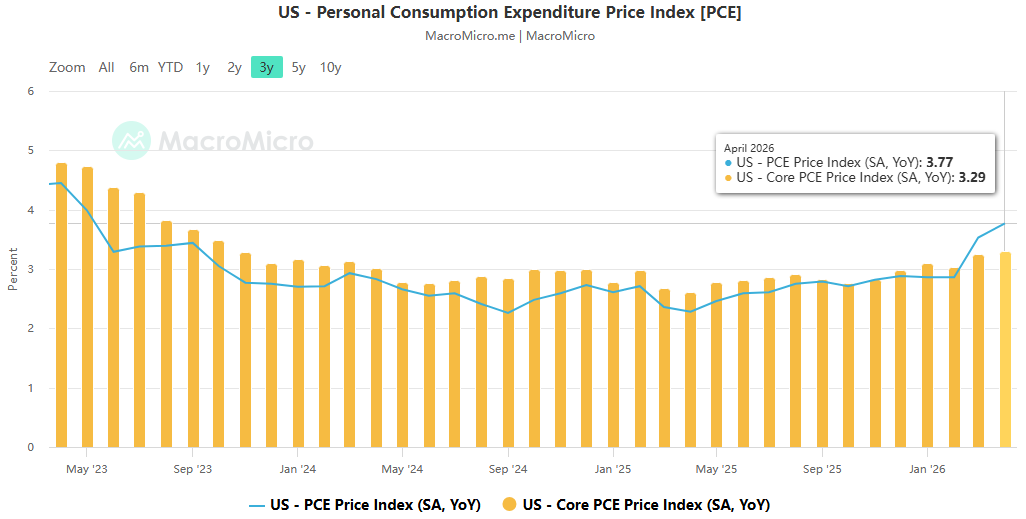

The ACE Markets policy research team believes this shift has a strong realistic background and logical support. From a theoretical perspective, inflation indices themselves involve numerous statistical assumptions and differences in methodology. For example, the calculation of owner-occupied housing inflation uses completely different statistical methods in the US and the Eurozone. Setting a rigid target for a number with room for subjective adjustment is inherently logically flawed. From a practical perspective, in April, the US PCE rose 3.77% year-on-year, and core PCE rose 3.29% year-on-year, significantly exceeding the 2% target for several consecutive years. The IMF has even postponed the point at which US inflation returns to 2% to the end of 2027. Rigidly adhering to numerical targets will either force central banks to excessively raise interest rates, shocking the economy, or continuously erode the credibility of monetary policy.

Looking back, this shift appears more like a correction of past policies. Before the pandemic, to compensate for inflation slightly below 2%, the Federal Reserve implemented a "flexible average inflation targeting" system, deliberately tolerating periods of inflation overshooting, which ultimately led to a once-in-forty-year high inflation shock. Had a more flexible "price stability" framework been adopted at the time, tightening could have been initiated earlier, avoiding the risk of subsequent runaway inflation. ACE Markets predicts that future Fed inflation decisions will no longer be solely anchored to the PCE figure, but will be based on a comprehensive assessment of a basket of price indicators, inflation expectations, and wage growth, significantly increasing policy flexibility. For the market, this also means that the traditional trading formula of "2% inflation triggering interest rate cuts" is completely ineffective, and the elasticity and volatility of inflation pricing will be amplified simultaneously.

III. Restructuring the Operational System: "Precise Slimming" of the Balance Sheet, Complete Iteration of the Balance Sheet Shrinking Logic

The third layer of the Walsh reform is the restructuring of the balance sheet management model, which is also the most fundamental operational support for monetary policy. Unlike the "scale of balance sheet reduction" that the market is generally concerned about, the core breakthrough of this reform lies in the complete change of the logic of balance sheet reduction—from the traditional "passive reduction of bond holdings and compression of reserve supply" to "reducing the demand for bank reserves and precisely optimizing the liability structure."

ACE Markets' policy research team estimates that the Federal Reserve's massive balance sheet has exposed four major problems: deep involvement in fiscal and credit allocation erodes the independence of monetary policy; becoming a fixed counterparty in the market weakens its financial intermediation function; squeezing the buffer space for balance sheet expansion during crises; and facing the risk of large book losses. However, calculations by researchers at the Milan Institute of the Federal Reserve indicate that reducing the balance sheet by $1 trillion to $2 trillion is entirely feasible and will not cause a drastic shock to the market. The core lies in the accompanying demand-side reforms: reducing banks' reliance on central bank reserves by simplifying discount window regulations, eliminating the "stigma" of the discount window, and adjusting policy interest rate spreads.

Given the current high supply pressure on US Treasury bonds and continued downward pressure on long-term yields, this balance sheet reduction path, which prioritizes reducing demand and secondarily reduces supply, is more moderate and can prevent a large influx of bonds into the market that could trigger a liquidity shock. ACE Markets believes that this reform will be implemented gradually and will not cause sharp fluctuations in the bond market in the short term. However, in the long run, a more streamlined balance sheet will restore the Fed's policy independence, reserving ample room for maneuver in the next cycle, and represents a substantial repair to the long-term health of monetary policy.

IV. Reshaping Trading Logic: The US Treasury Market is Entering Three New Paradigms

The systemic reforms spearheaded by Warsh are not merely policy and technical adjustments, but a reshaping of the underlying rules governing global asset pricing. ACE Markets' cross-cycle assessment model shows that the shift in three major trading paradigms is already gradually emerging in the market:

The main trading theme has shifted from "policy expectation game" to "high-frequency data game" . With the withdrawal of forward guidance, the market has lost a clear policy anchor. Every non-farm payroll, CPI, and PCE data release triggers a significant pricing correction. The weight of data-driven market movements has increased significantly, and the value of swing trading far exceeds that of trend holding.

Inflation pricing is shifting from "single-target anchoring" to "range-flexible pricing." 2% is no longer an absolute policy red line; the market's tolerance range for inflation will gradually widen, and fluctuations in inflation expectations will further amplify the elasticity of interest rate movements. The traditional linear logic of "interest rate cuts when inflation targets are met" no longer holds true.

Strategy preferences are shifting from "passive holding for easy profits" to "active management for profit." In a highly volatile environment, the uncertainty of capital gains from passively holding bonds has increased significantly, while the profit potential of active management strategies relying on swing trading and curve trading has expanded significantly. The "trading attribute" of the US Treasury market will be stronger than its "allocation attribute."

ACE Markets will continue to monitor three key milestones through its policy tracking matrix: signals of further adjustments to the communication mechanism at the July FOMC meeting, official documents and implementation timelines for inflation framework reform, and specific details and pace of the balance sheet reduction optimization plan, to help investors capture opportunities and risks in rule changes in real time.