summary:

As a professional institution deeply rooted in the global foreign exchange market, develop...

summary:

As a professional institution deeply rooted in the global foreign exchange market, develop...

As a professional institution deeply rooted in the global foreign exchange market, developed economy monetary policies, and cross-asset risk transmission, ACE Markets has long tracked the yen's exchange rate movements, the effectiveness of Japan's policy toolbox, and the spillover effects of carry trades on global equity markets. Recently, the Japanese Ministry of Finance has been promoting increased allocation of pension funds to domestic assets and expanding the scope of tax-free personal investments to support the yen and government bond markets. Meanwhile, the capital linkage between yen carry trades and US stock AI market trends continues to deepen, and these multiple factors have led to a continuous accumulation of hidden risks in the market. ACE Markets conducts a systematic analysis combining historical cycle patterns, capital structure data, and market microstructure to help investors understand the core logic and potential transmission paths.

The new policy on "capital repatriation" has a sound long-term logic, but its short-term effectiveness is limited.

Japanese Finance Minister Satsuki Katayama recently proposed encouraging large pension funds, such as the Government Pension Investment Fund, to increase their domestic asset allocation and include Japanese government bonds in the personal tax-free investment plan, attempting to support the government bond market and the yen exchange rate by guiding domestic savings back to Japan. The ACE Markets research team believes this policy direction is reasonable in the long term: Japan has a large domestic savings base, and if funds continue to be reallocated from overseas assets to the domestic market, it can provide a more stable demand base for Japanese government bonds and provide medium- to long-term support for the yen. However, based on our years of tracking and research on Japan's policy transmission mechanism, given that there has been no substantial shift in the current fiscal and monetary policy framework, such guiding policies are unlikely to have a decisive impact on market trends in the short term.

Based on market estimates, the increase in domestic bond holdings by government pension funds alone, reaching the upper limit of their allocation range, could generate approximately $76 billion in new government bond purchases. If pension funds, insurance companies, and retail investors are included, the potential inflow of funds could reach as high as $440 billion. However, we believe that a substantial scale does not equate to rapid implementation: a genuine policy impetus for fund repatriation depends on clarity regarding the fiscal path and the pace of interest rate hikes. Currently, the core pricing logic of the Japanese government bond market is still dominated by three variables: the contraction of central bank bond purchases, high levels of government debt supply, and the restructuring of term premiums. Policy statements primarily serve to guide expectations and have not yet changed the core operating logic of the bond market.

The marginal effect of foreign exchange market intervention is diminishing, and the policy toolbox still has shortcomings.

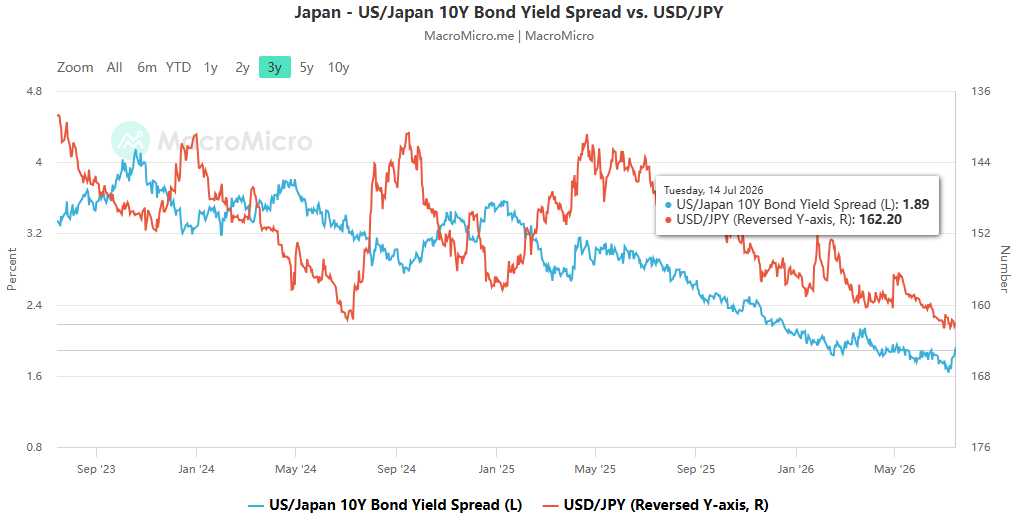

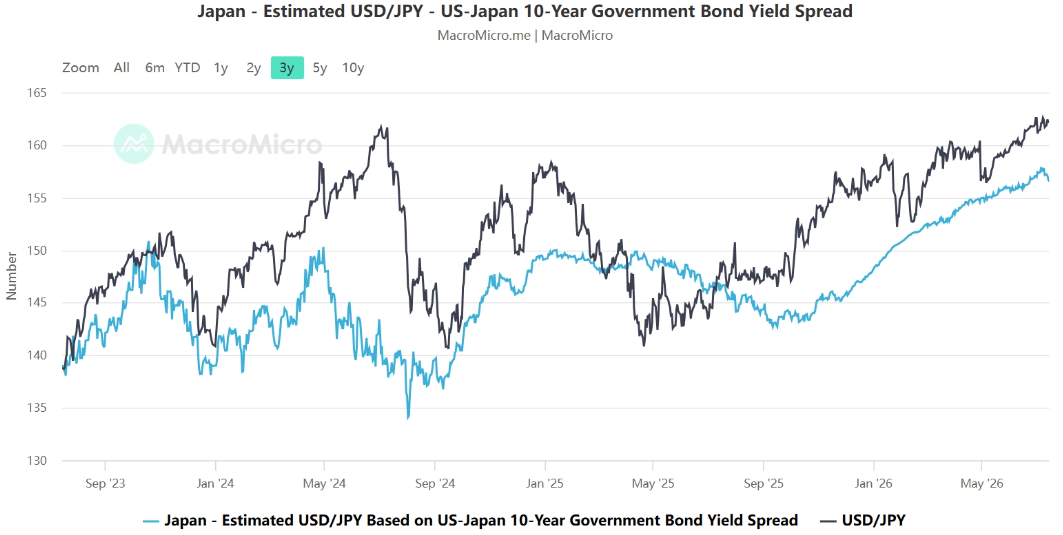

The Japanese authorities' push for the repatriation of domestic funds is essentially an attempt to find new leverage to support the yen and asset prices amid the continued weakening of the effectiveness of foreign exchange market intervention. So far this year, the Japanese government has injected a record 11.73 trillion yen into the market in an attempt to reverse the yen's weakness, but the yen remains near its lowest level against the dollar in nearly four decades, and the policy's effects have fallen short of expectations.

ACE Markets believes the core reason for the intervention's failure lies in the fact that two key market expectations have not reversed: first, the expansionary fiscal agenda of the Sanae Takaichi government has exacerbated market concerns about increased government debt supply; second, the market generally expects the Bank of Japan to only gradually normalize its policy, making it difficult for the Japan-US interest rate differential to narrow rapidly. Overnight index swap data shows that traders expect the Bank of Japan to raise interest rates by only 25 basis points this year, and the interest rate disadvantage is unlikely to improve significantly in the short term, fundamentally suppressing the yen's upside potential.

We further conclude that the statement regarding pension funds increasing their allocation to domestic assets leans more towards overall market expectation management than a strong stimulus policy specifically designed to support the government bond market. To some extent, it can be seen as an extension of "verbal intervention," aimed at maintaining the expectation of capital inflows rather than releasing large-scale purchasing power in the short term. In practical terms, such policies can only suppress the most aggressive speculative short sellers and cannot attract trend-following funds to go long on the yen. Essentially, they slow down the depreciation pace, rather than reverse the trend.

Underestimated micro-variables: Retail investor positions are reshaping the effects of policy intervention.

In tracking the micro-trading structure of the foreign exchange market, ACE Markets noticed a crucial variable that is easily overlooked: changes in the positions of Japanese retail investors have become an important factor influencing the effectiveness of policy intervention, and may even counteract the policy's effects. Data shows that, driven by rising expectations of foreign exchange market intervention, Japanese retail traders' net short positions in the US dollar have recently surged, more than tripling in a single month to reach 2.79 trillion yen, the highest level since records began in 2008.

Because the Japanese yen spot market has long been dominated by retail trading, this position structure of betting in the same direction directly dilutes the marginal effect of official intervention. When the market has already accumulated a large number of retail positions shorting the dollar and longing the yen, the incremental impact of official yen purchases will be significantly absorbed. More alarmingly, if intervention drives a rapid short-term appreciation of the yen, many retail investors will choose to close their positions to take profits, selling yen and buying back dollars, thus pushing the exchange rate back towards depreciation. Coupled with the rigid dollar buying by importers at low exchange rates, the combined effect of these two forces will quickly offset the effect of policy intervention. This logic has already been validated by the market: in May, the Japanese Ministry of Finance intervened with a record amount of funds, but the yen still depreciated by more than 4% from its pre-intervention high. The inverse relationship between retail positions and real demand is a significant reason why the intervention's effect fell short of expectations.

Risk spillover: The fragile resonance between yen carry trades and the US stock market's AI rally.

Leveraging its comprehensive market research framework covering foreign exchange, fixed income, and equities, ACE Markets has discovered that the yen's movements are not isolated foreign exchange market events. The underlying arbitrage trading chain is deeply intertwined with the current booming US AI stock market, creating a fragile resonance where "all prosper together, and all suffer together." This represents a hidden risk in the global equity market. Simply put, investors borrow low-interest yen, convert it into US dollars, and invest in risky assets like US stocks. Without currency hedging, they can simultaneously profit from interest rate differentials, asset appreciation, and dollar depreciation – this is yen arbitrage. The current surge in AI-related stocks has attracted significant arbitrage funds into US stocks, becoming a hidden source of capital driving up tech stock valuations. However, if the yen suddenly appreciates sharply, arbitrage trades will face concentrated liquidation, with funds rapidly withdrawing from risky assets, potentially triggering market corrections.

ACE Markets' analysis of the current market environment reveals that the USD/JPY pair is again hovering around the key 162 level, with market volatility at low levels. US stock market performance is highly concentrated in leading AI stocks, and the three-month implied correlation index, which measures the linkage between individual stocks and the index, is even lower than the same period in 2024, indicating that the market is severely under-pricing the risk of a systemic downturn. We believe that a single currency intervention typically only triggers short-term fluctuations and is unlikely to trigger a trend reversal. However, if catalysts emerge such as an unexpected interest rate hike by the Bank of Japan, fiscal tightening in Japan, or a significant increase in expectations of US interest rate cuts, a rapid appreciation of the yen will trigger a concentrated unwinding of carry trades. In a low-volatility, highly concentrated market environment, the impact will be further amplified, putting significant pressure on the US AI stock market.

Conclusion: Be wary of the dual fragility of narrative and funding.

ACE Markets adheres to a data-driven, end-to-end risk control research philosophy. We believe that while Japan's current policies to guide capital inflows have a long-term supporting logic, they cannot change the core operating trend of the yen and government bond markets in the short term. A deeper risk lies in the fact that yen carry trades have become a significant pillar of funding for global risk assets, and the optimistic narrative surrounding AI-driven market trends is deeply intertwined with cheap capital, leading to a continuous accumulation of vulnerability. For global investors, it is crucial to move beyond a single-market perspective and be wary of cross-asset risk transmission: tracking Japanese policy developments and changes in retail investor positions is essential, as is monitoring indicators such as US stock valuation concentration and implied volatility to guard against the impact of unexpected fluctuations.