summary:

Against the backdrop of uneven global economic recovery and intertwined external uncertain...

summary:

Against the backdrop of uneven global economic recovery and intertwined external uncertain...

Against the backdrop of uneven global economic recovery and intertwined external uncertainties, the recent monetary policy moves of the European Central Bank, the Bank of Japan, and the Federal Reserve are key indicators of the economic resilience and policy dilemmas of developed economies. Although the three central banks are at different stages of development—the Eurozone is showing initial growth momentum, Japan's moderate recovery harbors underlying weakness, and the US exhibits a "K-shaped" divergence—they all use interest rate adjustments as their core tool to balance inflation, growth, and external risks. Their decisions reflect their own fundamentals and, through exchange rates and stock markets, create global linkages. Internal disagreements also foreshadow future policy uncertainties.

Monetary policy choices: Maintaining stability as the primary goal, with divergent expectations regarding the path forward.

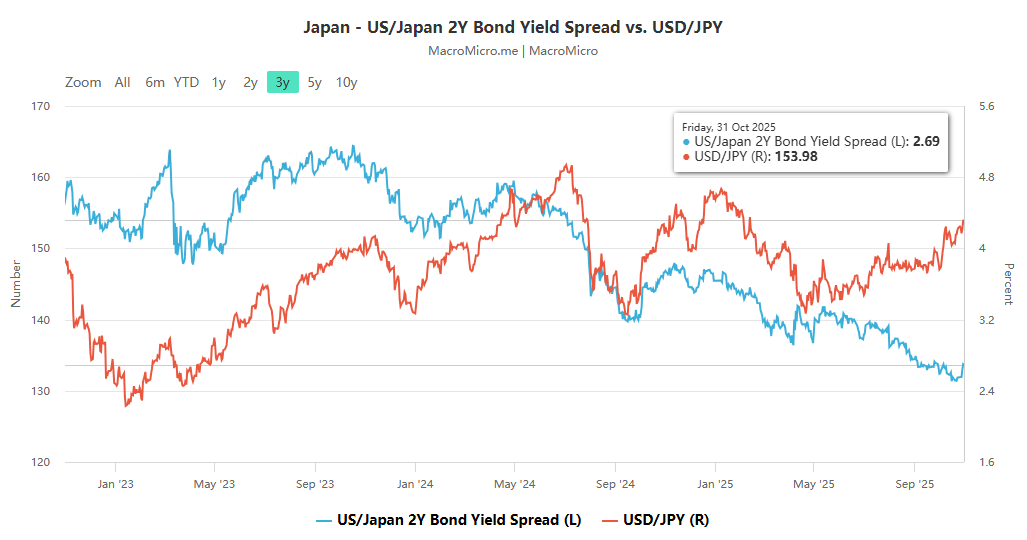

All three central banks have recently made "maintaining current interest rate levels" their main policy decisions, but the underlying policy intentions and future path expectations differ significantly due to their different economic stages, essentially reflecting a precise adaptation to their own fundamentals. The European Central Bank (ECB) has maintained its benchmark interest rate at 2% for three consecutive times, aligning with Lagarde's statement that "policy is in a good position." Supporting logic includes positive signals such as Q3 GDP growth exceeding expectations at 0.2% and inflation nearing the 2% target. The ECB has not signaled easing, extending its economic forecast period to 2028 to allow for adjustments. The Bank of Japan (BOJ) has maintained its interest rate at 0.5% for six consecutive times. The 7-2 vote highlighted inflation concerns, and the decision balanced risks such as a "moderate recovery" and weak exports, adopting a "cautiously accommodative" stance to leave ample room for future adjustments.

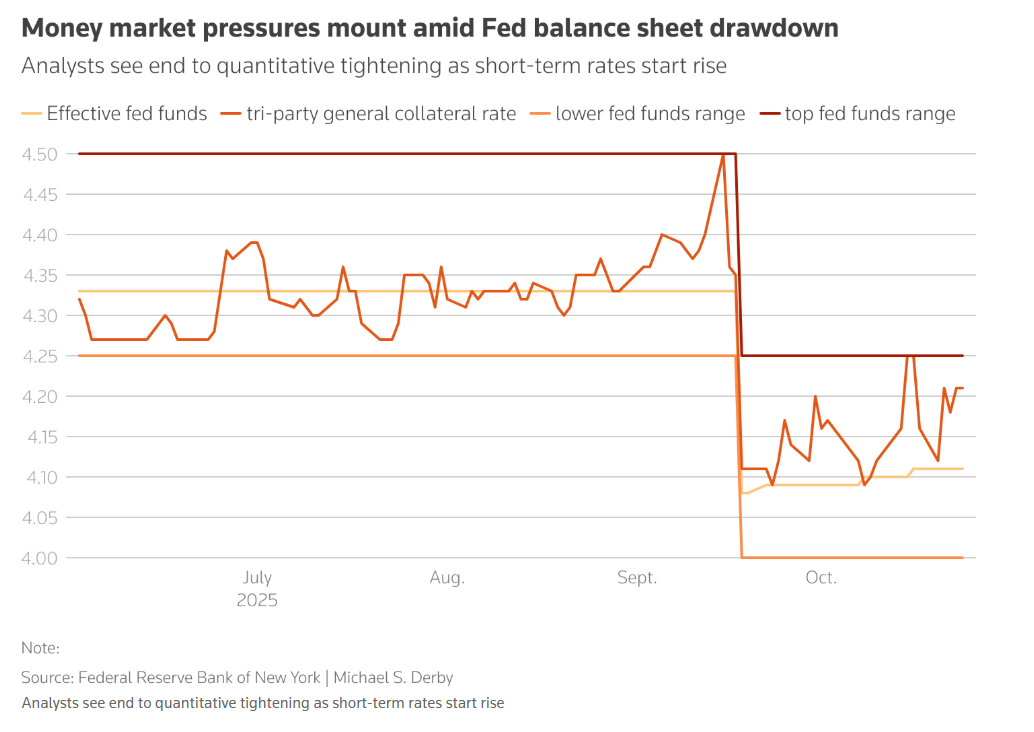

Unlike the European Central Bank and the Bank of Japan, the Federal Reserve's policy statements focused more on cooling market expectations for interest rate cuts. After a cumulative reduction of 150 basis points in the federal funds rate, Powell made it clear that another rate cut in December was "far from a done deal," and hinted that rate cuts would have limited impact on the labor market. The core reason lies in the complexity of the US economy: serious internal divisions among policymakers, insufficient data due to the government shutdown, persistently high inflation, and a labor market slowdown stemming from supply contraction rather than insufficient demand. This reflection on the limitations of policy tools broke the market's inertia of "continuous rate cuts."

The common logic behind the policies: the triple constraints of inflation, growth, and external risks.

Despite the different economic backgrounds of the three central banks, their decision-making processes all revolve around three core dimensions: "inflation target anchoring," "economic growth resilience," and "external risk resistance," highlighting the common challenges currently faced by central banks in developed economies.

Inflation target: close but not stable, uncertainty is key.

All three central banks use an inflation target of around 2% as their core anchor, but current inflation is showing a trend of "close to the target but unstable": the ECB believes inflation is close to the target but the outlook is uncertain, with concerns that defense spending will push up inflation in the medium term; the Bank of Japan predicts that core CPI will reach 2.7% in fiscal year 2025, then fall back to 1.8% in fiscal year 2026, indicating insufficient stability; and the Federal Reserve faces the reality of inflation consistently exceeding its target, which is key to its cooling of expectations for interest rate cuts. This "close but unstable" state puts central banks in a policy dilemma: tightening may stifle the recovery, while easing may trigger an inflation rebound, thus leaving them with only a "wait-and-see" balancing strategy.

Economic growth: Overall recovery coexists with internal divergence

All three central banks face "structural divergence amid overall recovery": France in the Eurozone is experiencing strong growth, while Germany remains sluggish; Japan is experiencing a "moderate recovery," but exports have contracted for four consecutive months (with only a slight rebound in September), and exports to the US are still declining; the US exhibits a typical "K-shaped divergence," with robust corporate investment and retail sales, but low- and middle-income groups are affected by shrinking labor supply, with the unemployment rate rising to a four-year high of 4.3%, the top 10% contributing half of consumption, and the wealth gap widening. This divergence limits the effectiveness of "one-size-fits-all" policies: the ECB needs to consider the differences between core and peripheral countries, the Bank of Japan needs to balance weak exports with domestic demand recovery, and the Federal Reserve needs to address the ethical dilemma that "stimulus policies only benefit the rich."

External risks: Global uncertainty becomes a common policy variable.

Global trade disputes, geopolitical tensions, and the spillover effects of US policy are common external variables affecting the decision-making of the three central banks: the ECB cited global environmental challenges, and BCA strategist Matthew Savari stated that European asset performance depends on US policy; the Bank of Japan is wary of trade uncertainties and the risk of US tariff transmission, and also faces pressure from the US regarding a weaker yen; the Federal Reserve's policy judgments are affected by the lack of data due to the government shutdown. The interdependence of the global economy makes it difficult for major central banks to act in isolation, and external risks have become a key factor constraining their policy space.

Market linkages and internal competition: the two-way transmission of policy effects

The monetary policy decisions of the three central banks not only directly affect their domestic financial markets, but also create global linkages through exchange rates, asset prices, and other channels; at the same time, the differences in policy stances within the central banks have further amplified market speculation about future paths.

Market Reaction: Exchange Rates and Stock Markets as a Barometer of Policy Effectiveness

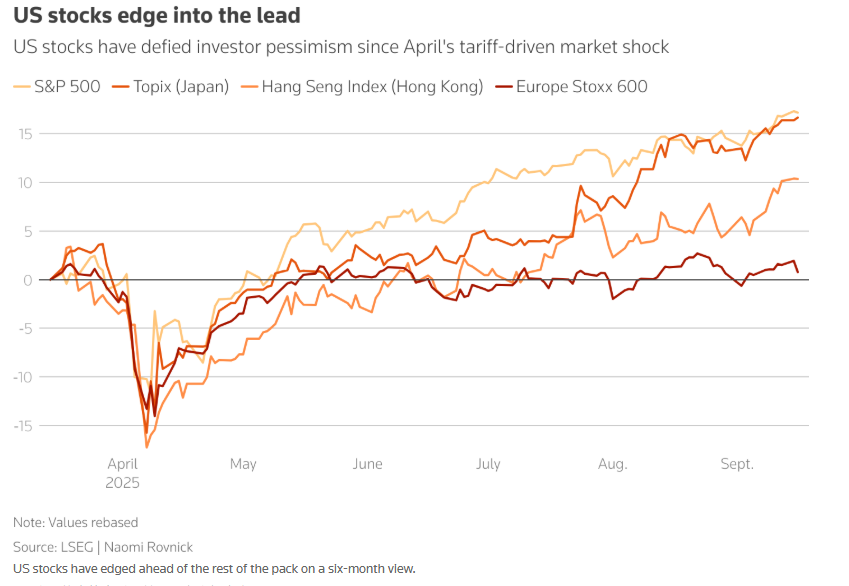

These reactions indicate that the market has developed a "pricing-inertia" for central bank policies, and even minor changes in policy signals can trigger significant adjustments in asset prices. Following the release of policy signals, market reactions closely mirrored policy intentions: after the ECB's decision, the euro rose slightly against the dollar, accumulating a 12% increase since 2025; after the Bank of Japan maintained its interest rate, the dollar rose about 70 points against the yen in the short term, the Nikkei 225 index rose slightly, and "high-market trading" pushed the index to a record high, while the yen fell below 150 against the dollar; Fed Chair Powell's "cooling-down" comments directly lowered expectations for a December rate cut, and asset price volatility subsided.

Internal divisions: The struggle between hawks and doves highlights the policy dilemma.

The three central banks all have internal policy stances diverging, primarily due to differing assessments of the relative importance of "inflation risk" versus "growth risk": The ECB's doves advocate for easing to address the risks of slowing growth and inflation (investors expect a 40-50% probability of a rate cut before next summer), while hawks favor the stimulus effect of German defense and infrastructure spending and oppose further easing; the Bank of Japan's 7-2 vote focused on "controlling inflation" versus "stabilizing recovery," with rate hike proponents concerned about rising prices, while the majority worried that rate hikes would suppress exports and domestic demand; the Federal Reserve's divisions are more complex, with some advocating for rate cuts to stabilize employment, while Powell and others believe that supply-side problems cannot be solved by demand stimulus and are wary of policy easing triggering bubbles. This divergence suggests that future central bank policies will be more "gradual," requiring more data verification to mitigate market volatility.

Future Outlook: Policy Anchors Amidst Uncertainty

Combining the decisions and statements of the three central banks, the future monetary policies of developed economies will be characterized by "stability as the main focus, with adjustments made as needed." The core anchors include verification of economic data, response to external risks, and policy coordination. These monetary policy choices are essentially responses to their own fundamentals and "cautious testing" under global uncertainties. Against the backdrop of unstable inflation, economic divergence, and lingering external risks, their policies will maintain a "stable yet flexible" characteristic. The linkage effect and internal game will continue to shape the global financial market. For market participants, paying attention to the interpretation of central bank data and changes in policy stance is key to seizing opportunities and avoiding risks.